Navigating Health Reimbursement Arrangements (HRAs) for Small Businesses

For many small employers, offering health benefits usually isn’t a federal legal requirement—but it can be a major lever for recruiting and retention. (Different rules apply to larger employers.) Under the ACA’s employer shared responsibility rules, the requirement to offer coverage generally applies to Applicable Large Employers (ALEs): employers that averaged at least 50 full-time employees (including full-time equivalents) in the prior calendar year.

It's also the key to attracting top-notch talent, optimizing employee retention, and improving productivity in the workplace.

This leads us to Health Reimbursement Arrangements (HRAs): an employer-funded health benefit arrangement that has been growing in popularity as federal rules expanded options like QSEHRAs and ICHRAs.

In this post, we'll take a look at HRAs, why they're gaining popularity, how they work, and tips to implement them successfully for small businesses.

But before we go any further, a quick introduction.

What are HRAs?

A Health Reimbursement Arrangement (HRA) is an employer-funded benefit arrangement that reimburses employees for qualified medical expenses up to a maximum dollar amount for a coverage period (often designed and communicated as a monthly allowance). Whether premiums are eligible depends on the HRA type and plan design. Reimbursements are generally tax-free when the plan rules are met and claims are properly substantiated.

There are different types of HRAs suited to the needs of small businesses, namely;

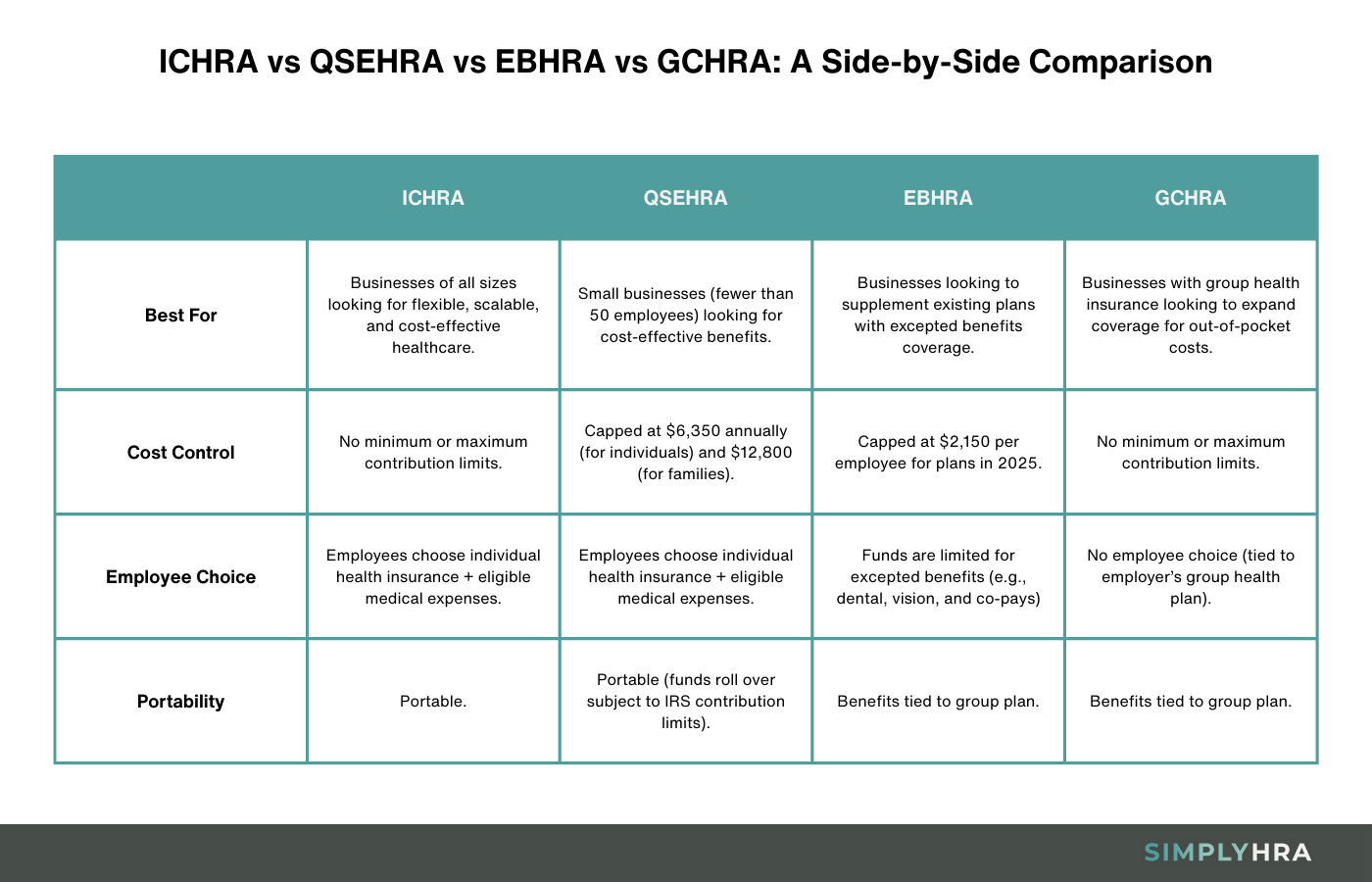

- Individual Coverage Health Reimbursement Arrangement (ICHRA)

- Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

- Excepted Benefit Health Reimbursement Arrangement (EBHRA)

- Group Coverage Health Reimbursement Arrangement (GCHRA)

Each HRA type comes with unique features, benefits, and disadvantages. As premiums and plan choices continue to change across the individual and group markets, many small employers are exploring HRAs as a way to control costs while giving employees more plan choice.

Benefits of HRAs for Small Businesses

Here's a quick look at the advantages of choosing an HRA for your business:

- Cost control — Employers set the allowance for any HRA. Some HRAs also have statutory annual caps (notably QSEHRA and EBHRA). ICHRA does not have a statutory cap (the employer sets the amount), and integrated/group HRAs also typically rely on employer-set limits.

- Flexibility — QSEHRA and ICHRA can give employees choice over individual coverage and eligible expenses. However, HRAs and HSAs interact: many HRAs that reimburse medical expenses can make someone ineligible to contribute to an HSA unless the HRA is designed to be HSA-compatible (for example, limited-purpose or post-deductible).

- Tax benefits — Employer HRA reimbursements are generally deductible, and reimbursements are generally tax-free to employees when the HRA rules are satisfied (for example, under an ICHRA the employee must be enrolled in individual health insurance or Medicare for each month they’re covered by the ICHRA).

- Better employee satisfaction — With the right approach, an HRA can do a better job at keeping employees energized, healthy, and motivated to contribute to your startup's growth. It's all about learning their needs and providing them with sufficient training on making the most out of their benefits.

While certain types of HRAs have unique advantages over others, HRAs are generally seen as less risky and more flexible for employers than other healthcare options.

To make the best choice for your business, it's crucial for you to understand what makes each HRA different.

Types of HRAs

Without further ado, here's a closer look at the different HRA types that work great for small businesses:

1. Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

QSEHRA is a type of HRA designed for eligible small employers—generally employers that are not Applicable Large Employers (ALEs) and don’t offer a group health plan. Employers can also exclude certain categories of employees allowed under federal rules (for example, employees who haven’t completed 90 days of service, part-time or seasonal employees, employees under age 25, union employees covered by a CBA, and certain nonresident aliens). It allows employers to reimburse eligible employees for qualified medical expenses (including individual health insurance premiums) up to an IRS-indexed annual maximum, and it must be offered on the same terms (with limited permitted variations, such as by age and family size, within federal rules). Reimbursements are generally tax-free only if the employee has minimum essential coverage (MEC) for the months reimbursed.

Some of the defining characteristics of QSEHRA are:

- Replace with single, accurate statement: 'For plan years beginning in 2026, the indexed QSEHRA limits are $6,450 (self-only) and $13,100 (family coverage).'

- Must be offered on the same terms to all eligible employees, but the permitted benefit may vary by age and family size within federal rules

- Employees can choose the medical services and insurance products they need

These features streamline the administration of QSEHRA plans for small businesses. However, they also add restrictions to what otherwise would've been a highly flexible and infinitely scalable healthcare solution. Employers offering a QSEHRA must generally provide a written notice to eligible employees, typically at least 90 days before the start of the plan year, or when an employee becomes eligible.

2. Individual Coverage Health Reimbursement Arrangement (ICHRA)

Individual Coverage Health Reimbursement Arrangement (ICHRA) is a newer HRA type that addresses some of the limitations of QSEHRA.

For starters, it is available to employers of any size — whether you have only one or hundreds of employees in need of healthcare. To participate, employees must be enrolled in individual health insurance (on or off an Exchange) or Medicare for each month they’re covered by the ICHRA; short-term limited duration insurance (STLDI) and coverage consisting solely of excepted benefits (like dental/vision-only) don’t satisfy this requirement.

Employers can offer ICHRA by employee class, but they must offer it on the same terms to everyone within a class (amounts may be increased for older employees and for employees with more dependents, within federal rules). Generally, employers can’t offer employees in the same class a choice between a traditional group health plan and an ICHRA—though employers may offer ICHRA to some classes and traditional group coverage to other classes, subject to federal class rules and (in certain situations) minimum class size requirements.

ICHRA also doesn't have annual contribution limits, enabling companies to offer coverage options that can match a wide range of healthcare needs. And, unlike QSEHRA, your ICHRA strategy can include different reimbursement plans per employee group or class.

Premium tax credits: Being offered an ICHRA can affect whether an employee can get ACA premium tax credits. If the ICHRA offer is considered affordable under federal rules, the employee generally isn’t eligible for premium tax credits for Marketplace coverage for that period.

3. Excepted Benefit Health Reimbursement Arrangement (EBHRA)

EBHRA stands for Excepted Benefit Health Reimbursement Arrangement.

An Excepted Benefit HRA (EBHRA) is a limited HRA offered in addition to a traditional group health plan. It can reimburse certain out-of-pocket costs and may reimburse premiums for excepted benefits (like dental/vision) and short-term, limited-duration insurance (STLDI). However, EBHRA generally cannot reimburse premiums for individual health insurance, Medicare, or group health plan premiums (other than COBRA).

Note: Under current federal rules, STLDI sold or issued on/after September 1, 2026 is limited to an initial term of no more than 3 months and a maximum duration of no more than 4 months (including renewals/extensions), and state rules may be stricter—confirm current federal and state limits before relying on STLDI.

4. Group Coverage Health Reimbursement Arrangement (GCHRA)

A group-integrated HRA (often called a Group Coverage HRA) is designed to work alongside an employer’s group health plan and reimburse eligible out-of-pocket medical expenses (for example, deductibles and copays). It generally cannot reimburse individual health insurance premiums. There isn’t typically a separate statutory cap like QSEHRA/EBHRA, but the employer sets the plan’s reimbursement limit.

HSA note: If an employee is covered by an HDHP, a general-purpose HRA that reimburses medical expenses can generally make the employee ineligible to contribute to a Health Savings Account (HSA), unless the HRA is structured to be HSA-compatible (for example, limited-purpose or post-deductible).

How to Implement an HRA for Small Businesses

Ultimately, each HRA type comes with its own set of pros and cons.

Your goal is to pick the healthcare plan that aligns with your business objectives, employee needs, and budget.

Here's a step-by-step strategy that will help you achieve this:

1. Start With Your Business Needs

A successful small business healthcare strategy begins and ends with your employees.

You need to ask questions like, what are your workforce's demographics? What are their healthcare needs?

Furthermore, does your company have (or has access to) the resources to implement the ideal healthcare plan?

At this point, you can still choose non-HRA options like a traditional small-group health plan (including SHOP where available) or alternative funding approaches such as level-funded arrangements, each with tradeoffs in cost predictability, flexibility, and administration.

2. Decide Your HRA Type

If you're determined to adopt an HRA for your business, the next step is to decide which type to use.

EBHRA and GCHRA are useful if you have an existing, employer-sponsored health plan. Both can augment plans by providing additional coverage, with GCHRA specifically designed for group health plans.

QSEHRA and ICHRA, on the other hand, are ideal for providing flexible and predictable healthcare reimbursement allowances for small businesses without group plans.

ICHRA, however, is the better choice if you're after total control and predictability of costs.

Without annual contribution limits and employer size requirements, you have complete freedom to create a healthcare plan tailored to your workforce.

3. Set Your Budget

After deciding your HRA type, the next step is to set your monthly reimbursement budget.

Don't forget that your goal here is to strike the balance between employee needs and your company's financial stability.

Start by assessing your financial capacity, evaluating factors like cash flow, revenue, and — if applicable — the costs of existing benefits. Then, calculate the costs of your employees' healthcare needs, including health insurance premiums and common out-of-pocket medical expenses.

Be sure to factor in the tax advantages of HRAs when defining your reimbursement allowances. Generally, employer contributions to an HRA are deductible business expenses, and employee reimbursements are generally tax-free when the HRA’s requirements are met (for example, ICHRA requires substantiated enrollment in individual coverage/Medicare).

If your financial capacity and employee healthcare needs don't align, consider building your initial plan around high-priority medical expenses first. Communication with employees is key here, which leads to the next step.

4. Communicate With Employees

Employee communication and collaboration are important elements of HRAs — before and after implementation.

During the planning stage, give employees the opportunity to voice their health concerns and needs, especially while performing work-related duties. This ensures you set adequate reimbursement allowances that will keep them healthy and motivated in the workplace.

After launching your HRA, communication should revolve around educating employees about their benefits. This should include the eligible medical expenses covered by your HRA and the tools they need to request reimbursements.

Effective communication should also persist while your HRA is ongoing. This is to ensure employees are satisfied and confident with their coverage.

5. Launch, Monitor, and Adjust

With your HRA up and running, your focus should shift into tracking and optimizing your strategy based on a handful of metrics, like:

- Participation rate — The percentage of eligible employees who are actually enrolled in your HRA. A lower participation rate may indicate problems in terms of communication, plan structure, and the sufficiency of reimbursement allowances.

- Utilization rate — The portion of the available allowance that is actually used for reimbursements (for example, reimbursements paid as a percentage of the maximum amount made available).

- Administrative costs — The direct costs of managing your HRA. Depending on your setup, this may include platform subscriptions and third-party administrator fees.

- Employee retention rate — Believe it or not, employee health benefits have a direct impact on employee retention. Monitoring employee retention rate over time, especially after implementing your HRA, is a great way to gauge its effectiveness through the lens of your workforce.

Tracking these metrics is your gateway to making sharper, data-driven decisions on employee healthcare. At the same time, stay open to employee feedback to identify improvement opportunities that the numbers don't tell you.

For example, when running an ICHRA plan, employees may find it challenging to pick an individual health insurance plan on their own.

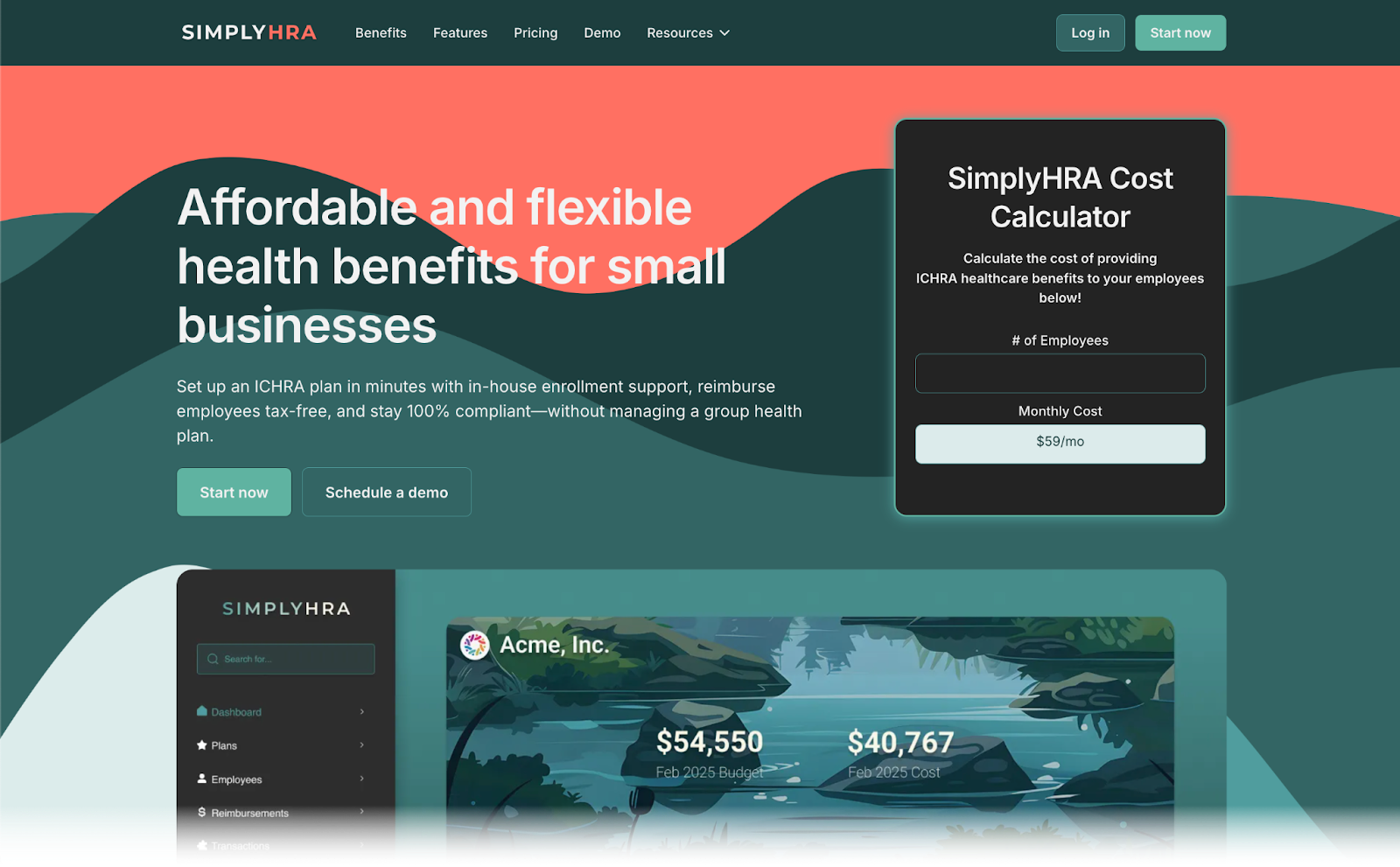

With platforms like SimplyHRA, you can streamline the insurance plan selection process by providing recommendations that are compatible with your ICHRA plan.

As a software solution specifically designed for ICHRA, SimplyHRA also comes equipped with an AI chatbot that can accelerate employee training. It can answer HRA-related questions, provide reimbursement status updates, share instructions on plan management tasks, and more.

Common HRA Challenges

Apart from employee training, here are other common challenges associated with implementing an HRA for small businesses:

- Regulatory compliance — Navigating IRS and Affordable Care Act (ACA) rules can prove to be a significant roadblock when it comes to adopting HRAs. The challenge includes drafting plan documents that outline essential information for compliance, such as written privacy procedures, eligibility requirements, reimbursement claims procedure, plan administrators, and other provisions for federal acts (e.g., the Health Insurance Portability and Accountability Act HIPAA and Employee Retirement Income Security Act ERISA).

- Administrative burden — As a self-funded plan, employers are primarily responsible for administrative tasks like substantiating eligible claims (for example, verifying qualifying expenses and/or premium documentation, depending on the HRA type) and reviewing reimbursement requests. Thankfully, this can be offset by working with a third-party HRA administrator or choosing a managed software solution.

- Budget constraints — HRA types with annual contribution limits (e.g., QSEHRA and EBHRA), might be insufficient to cover all of the healthcare needs of your employees. This can be addressed by combining your limited HRA with other health benefits or choosing a model without contribution limits (i.e., ICHRA).

Another challenging aspect of HRAs is choosing a Third-Party Administrator (TPA) or administration platform.

Remember, your choice will have a direct impact on the costs, dependability, and effectiveness of your HRA plan. It also affects how you can overcome challenges like regulatory compliance, managing reimbursements, and setting your budget.

Top HRA Administration Platforms

The good news is, you don't have to start from scratch when researching HRA administration solutions.

Below, we compiled five HRA administration platforms that can help streamline setup and ongoing compliance. Pricing changes frequently—confirm on each provider’s pricing page:

1. SimplyHRA

HRA Types: ICHRA

Price (as of February 2026): $29 per month per employee

Key Features:

- Reimbursement workflow + audit-ready reporting

- AI chatbot for employer/employee benefit Q&A

- Desktop and mobile app versions

Developed specifically for ICHRA, SimplyHRA consolidates everything you need into a single intuitive platform. It allows you to create multiple plans for different employee groups, onboard members, manage reimbursements, and track analytics — all in one dashboard.

Click here to schedule a personalized demo.

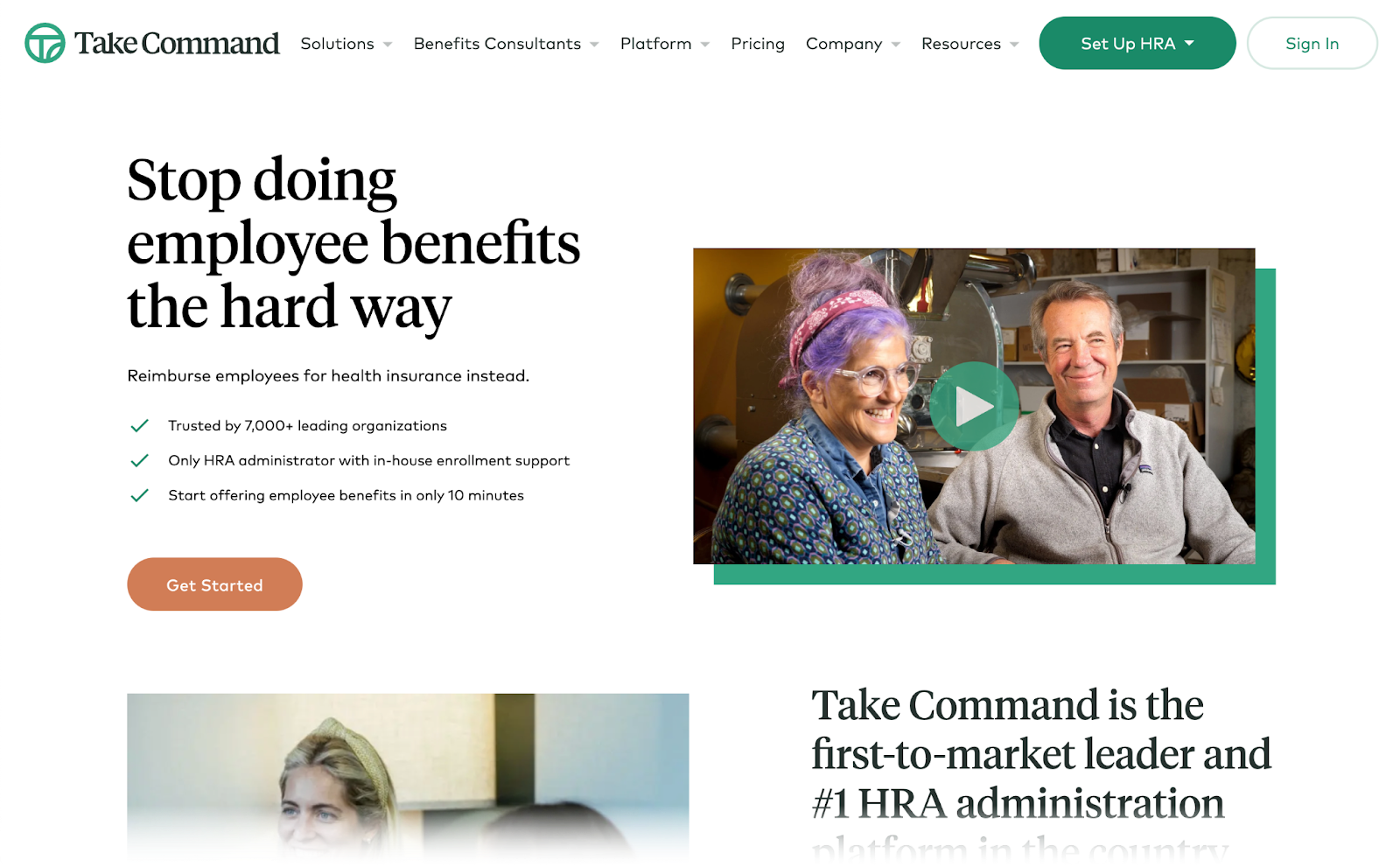

2. Take Command

HRA Types: ICHRA and QSEHRA

Pricing as of February 2026:

- Small employers: $20+ per employee per month plus $40+ monthly platform fee;

- Large employers: custom plus $100+ monthly platform fee

Key Features:

- HRA Hub platform designed for customizability

- Managed employee onboarding assistance

- AutoPay tool for automating monthly insurance premiums

Take Command is a trusted QSEHRA + ICHRA administration solution that can deliver a custom-designed HRA management portal. The company also offers managed services for onboarding employees and completing compliance requirements — handing off HRA reports to your accounting department or payroll specialist each month.

3. StretchDollar

HRA Types: ICHRA

Pricing as of February 2026: $40 base fee per month + $8 per month for each active employee

Key Features:

- Hands-off management

- Automatic payments for premium reimbursements

- Simple setup

StretchDollar is an ICHRA administration service that makes the process as streamlined and painless as possible.

After a few minutes of setup (including specifying your budget), the rest will be handled by the StretchDollar team. They will be in charge of all the heavy lifting, including reimbursement management and compliance.

4. PeopleKeep

HRA Types: ICHRA, QSEHRA, and GCHRA

Pricing as of February 2026: ICHRA starting at $25 per employee per month + a $50 monthly base fee - minimum of 3 seats.

Key Features:

- Design your own benefits

- Auto-generated plan documents

- Expedited employee onboarding

PeopleKeep is another well-known HRA administration software, which supports three of the top HRA types: ICHRA, QSEHRA, and GCHRA. The platform is designed to turn several hours of HRA administration into a few minutes of navigating a visual dashboard, which includes analytics reports and a detailed reimbursement tracker.

5. Salusion

HRA Types: EBHRA, GCHRA, QSEHRA, and ICHRA

Pricing as of February 2026: $14 per employee per month (ICHRA and QSEHRA) or $5 per employee per months (EBHRA and GCHRA)

Key Features:

- Managed compliance and plan documentation

- Expense validation via web portal and mobile app

- Direct payments to individual and group insurers

Salusion is a lightweight HRA administration software with basic features for all HRA types. In addition to automating tasks related to compliance and plan documentation, the platform also helps with expense verification, reimbursement approvals, and reporting through a clean app interface.

Conclusion

Conducting research is the first step to implementing a successful HRA plan for your small business.

You need to be familiar with the different HRA types, their unique advantages, and the necessary steps for implementation. More importantly, you need to find the ideal HRA administration solution that matches your needs.

SimplyHRA helps streamline key workflows—plan setup, employee onboarding, reimbursements, and reporting—while employers remain responsible for offering the benefit in compliance with applicable federal rules. Contact us for a private 1:1 consultation.

Related blogs

QSEHRA Plan: 2026 Rules, Limits, Eligibility & Taxes

1094-C vs 1095-C: ACA Employer Reporting Guide 2026