Your ICHRA Questions, Answered

We’ve helped dozens of small businesses switch to ICHRA. Here are the questions they ask most—and the honest answers we give on every consultation call.

General HRA FAQs

Why choose an ICHRA over a traditional group plan?

An ICHRA offers flexibility, predictable costs, and personal choice. Employers control their budget, and employees pick coverage that fits their needs.

Is it difficult to switch from a group plan to ICHRA?

Transition is generally straightforward. Once your group plan ends, employees can move to individual coverage, often using a special enrollment period tied to the termination of the group plan.

What does “qualifying individual health coverage” mean?

Qualifying coverage typically includes ACA marketplace plans, private individual plans, or Medicare. Short-term plans or sharing ministries are usually excluded.

Are there minimum or maximum contribution limits for ICHRA?

There’s no set limit from the IRS. Employers can choose the amount that fits their budget and can adjust it annually if needed.

Do all states recognize ICHRA?

ICHRA is a federal arrangement recognized in all 50 states. However, insurance options and costs may vary based on state regulations and marketplace availability.

How does SimplyHRA ensure privacy and security?

We use industry-standard security protocols and encryption to protect sensitive data. Only authorized individuals have access to personal and reimbursement information.

What if an employee has coverage through a spouse’s plan or other means?

Coverage under a spouse’s employer group plan does not satisfy the individual-coverage requirement for ICHRA participation. To receive ICHRA reimbursements, the employee must be enrolled in qualifying individual health insurance or Medicare. An employee who has other coverage may decline the ICHRA.

Do employees need to re-enroll every year?

Employees with continuous coverage typically don’t need to re-enroll in the ICHRA itself. However, it’s wise to review plan options annually—especially if your employer adjusts reimbursement amounts or if your insurance needs change.

Can employers use an ICHRA to satisfy ACA employer mandate requirements?

Yes, for certain employers. If you are an Applicable Large Employer (ALE), an ICHRA can be structured to meet ACA affordability requirements. SimplyHRA helps check for compliance before finalizing plan details.

What kind of support does SimplyHRA offer if I need help?

We provide customer support via email, phone, and live chat to answer questions about set-up, compliance, and everyday use. Our goal is to make offering and managing an ICHRA as simple as possible.

How do I get started with SimplyHRA?

Simply have your employer create an employer account at SimplyHRA.com and have them invite you to their team. Once invited, the platform guides you step-by-step through your healthcare plans, reimbursements, and more. If you have any other questions, please contact SimplyHRA.

Still have questions?

Can’t find the answer you’re looking for? Contact us! We're here to help.

HRA FAQs for Employers

What is ICHRA, and how does it benefit my business?

ICHRA (Individual Coverage Health Reimbursement Arrangement) lets you reimburse employees for health insurance premiums (and optionally medical expenses) on a tax-free basis. It can be more cost-effective than a group plan and offers flexible coverage options for employees.

Is providing an ICHRA legal and compliant?

Yes. Federal final rules establishing ICHRAs were issued in 2019, and employers could first offer them for plan years beginning January 1, 2020. Compliance depends on how the ICHRA is designed and administered, including coverage substantiation, notices, plan terms, and any applicable ACA employer-mandate requirements.

How do I set a budget for my employees’ reimbursements?

You decide how much to reimburse—there’s no minimum or maximum. You can even set different reimbursement amounts for different classes of employees (e.g., part-time, full-time, or by location). SimplyHRA will help every step along the way.

Can I contribute different amounts to different employees?

Yes. You can create separate “classes” (e.g., full-time vs. part-time) and allocate reimbursement amounts accordingly, as long as you comply with the rules for defining these classes.

Will I have to handle any claims or paperwork?

No. SimplyHRA automates claim submissions and reimbursements. You set your plan parameters, and our platform handles the paperwork for you.

How does offering ICHRA impact my taxes and my employees’ taxes?

Employer reimbursements are generally tax-deductible as a business expense. Employees receive reimbursements tax-free, provided they hold qualifying individual health insurance.

How do I know if ICHRA is right for my company compared to a traditional group plan?

If you value budget control and want employees to pick their own coverage, an ICHRA may be a better fit. For employers who prefer a single group plan with standardized coverage, a traditional plan could be considered—but often at a higher cost.

What if an employee doesn’t buy health insurance at all?

Employees must have qualifying coverage to receive reimbursements. If they opt out or do not enroll, they won’t be reimbursed. SimplyHRA only pays for valid expenses, so there’s no cost to you for employees who remain uninsured.

How do I get started with SimplyHRA?

Sign up at SimplyHRA.com, create your employer account, and set your reimbursement rules. The platform guides you step-by-step through defining budgets, classes, and compliance details. If you have any other questions, please contact SimplyHRA.

Still have questions?

Can’t find the answer you’re looking for? Contact us! We're here to help.

HRA FAQs for Employees

What is ICHRA, and how does it help me as an employee?

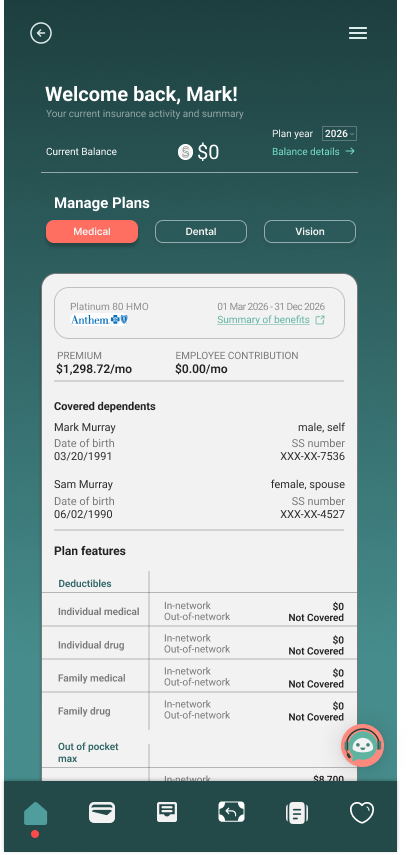

With ICHRA, your employer reimburses you for health insurance premiums (and possibly medical expenses). You choose your own plan, which can be a marketplace plan or private coverage, and get reimbursed for the portion your employer sets.

Do I need to buy a specific health plan?

You need to choose a qualifying individual health insurance plan. This can include ACA marketplace plans, private plans, or Medicare (if eligible). Short-term or health sharing ministry plans typically do not qualify.

How do I get reimbursed for my premiums or medical expenses?

You’ll submit proof of payment (such as receipts or statements) through the SimplyHRA platform. Once verified, your employer reimburses you up to the set allowance.

Is there a deadline to enroll in a health plan to use ICHRA?

Generally, you need to enroll in a plan during the ACA’s open enrollment or a special enrollment period (e.g., loss of other coverage). However, ICHRA itself often triggers a special enrollment period, allowing you to sign up for coverage outside standard open enrollment windows.

Do I pay taxes on my ICHRA reimbursements?

No. As long as you have a qualifying health plan, your employer’s reimbursements for premiums and/or medical expenses are tax-free.

Can I use ICHRA to cover my family’s premiums too?

It depends on whether your employer’s ICHRA plan design includes family coverage. If it does, you can be reimbursed for premiums covering your spouse and dependents, provided they have qualifying coverage.

What happens if I switch jobs or leave the company?

The individual insurance policy is separate from the ICHRA and may continue if you keep paying its premium. Your active-employee ICHRA coverage normally ends under the plan’s terms, but if the employer and plan are subject to federal COBRA, termination of employment or a reduction in hours that causes a loss of ICHRA coverage may give you or another qualified beneficiary the right to continue the ICHRA, generally at your own expense.

What if my premiums exceed the monthly reimbursement amount?

Any costs over your employer’s monthly allowance are your responsibility. You’ll pay the difference out of pocket.

Will SimplyHRA help me pick a health plan?

While SimplyHRA doesn’t directly select a plan for you, our platform provides resources and tips to help you find the right coverage. If you need personalized advice, you can consult a licensed insurance broker or use the ACA marketplace.

How often can I change my health plan?

You can typically change your plan during the ACA’s open enrollment period or if you experience a qualifying life event (e.g., marriage, birth of a child). However, keep an eye on enrollment deadlines to ensure you stay covered.

How do I get started with SimplyHRA?

Simply have your employer create an employer account at SimplyHRA.com and have them invite you to their team. Once invited, the platform guides you step-by-step through your healthcare plans, reimbursements, and more. If you have any other questions, please contact SimplyHRA.

Still have questions?

Can’t find the answer you’re looking for? Contact us! We're here to help.

Ready to provide the best health benefits experience to your employees?

Schedule a free 15-minute consultation. We’ll walk you through pricing, the virtual card, and exactly how setup works—no commitment required.

Happier employees

Easy to setup

Tax-free savings