Ditch the Group Plan. Switch to ICHRA In Minutes.

Set up ICHRA and start enrolling your team into qualifying individual or family coverage in minutes. Give every employee a fixed, tax-free monthly budget via a SimplyHRA virtual card to buy and pay for the individual coverage that fits their doctors, family and life. You get the tax benefits, compliance, and administrative relief of an ICHRA administrator.

Flat $29 per employee per month with a 60-day moneyback guarantee. No platform fees. No setup fees. No consultation fees. No HSA fees.

Everything you need to offer amazing health benefits to your team.

SimplyHRA makes it easier to offer personalized healthcare to your employees. Set your budget. Employees pick their plans. We handle the rest.

Cost control

Set a fixed monthly budget per employee class. Your cost is locked. No annual renewal surprises. Employer contributions are a pre-tax business deduction.

Employee choice

Each employee picks the plan that fits their doctors, prescriptions, and family. Assign different plans to employees in different states. No more one-network-fits-all.

Virtual card

Every employee gets a pre-funded virtual card loaded with your monthly contribution. It pays the insurance premium directly. No reimbursement forms, no 4-week waits.

Compliance

We generate plan documents, ICHRA notices, tax documents, and ACA-ready reports so you stay compliant without becoming a benefits expert.

Benefits specialist

Every employee gets access to a licensed, local benefits specialist who helps them compare plans and enroll at no extra cost. No more navigating Healthcare.gov alone.

Plan flexibility

Structure your HRA to reimburse eligible premiums and medical expenses. To preserve HSA eligibility, use a premium-only, limited-purpose, or post-deductible design. Any employer HSA contributions are made separately from the HRA.

Your benefits under control

A self-serve platform for employers and employees—with real human support whenever you or your colleagues need it.

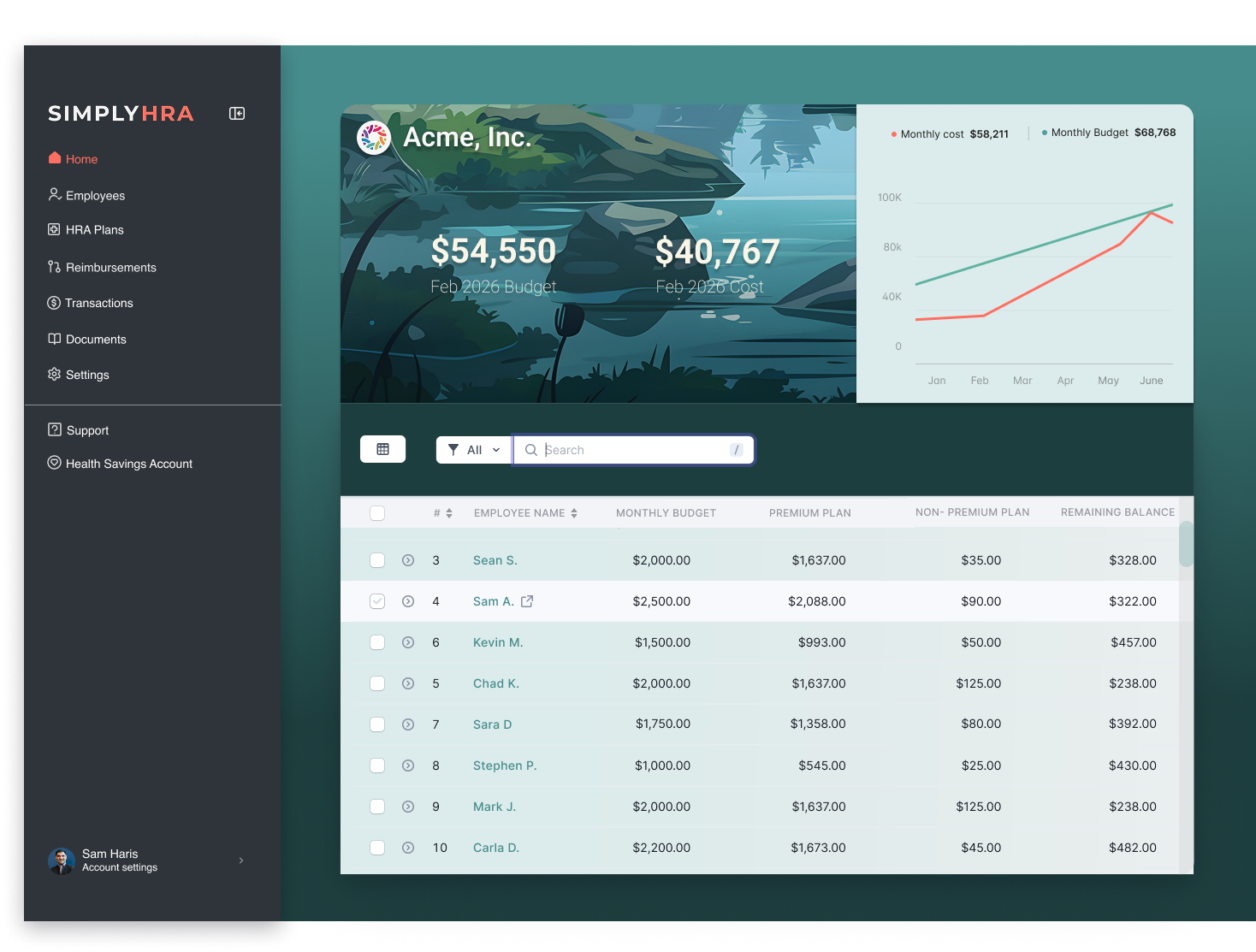

Set Your Budget & Fund Cards In Minutes

Choose how much to reimburse per employee class (full-time, part-time, by location). No minimums, no maximums. Change it annually as your budget grows.

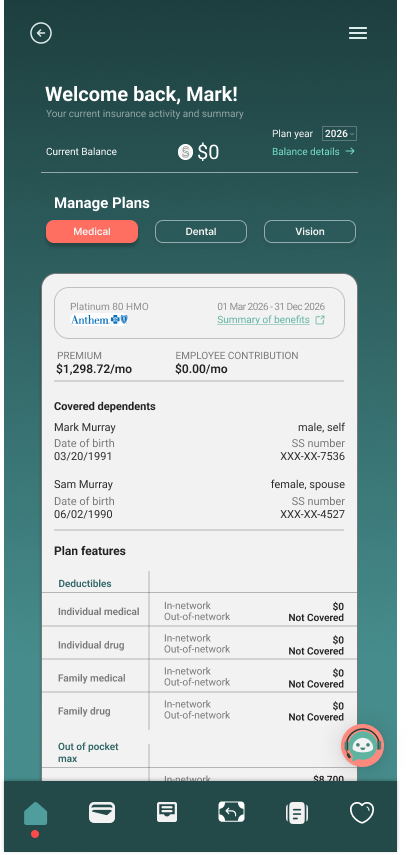

Employees Pick Plans That Fit Their Lives

A licensed benefits specialist helps each employee compare ACA marketplace and private plans that can cover their doctors, prescriptions, and family. Included at no extra cost.

Virtual Cards Handle Payments

Each employee gets a pre-funded virtual card that pays their insurance premium directly. Employees then upload proof of payment to SimplyHRA for compliance and approval.

Ongoing Personalized Support via Email, Call, or Text.

Our team and AI assistant help with eligibility questions, plan changes, regulations, and compliance via email, phone, or chat so neither you nor your employees are ever stuck.

Simple and transparent pricing

No setup fees. No onboarding fees. No platform fees. No switching fees. One price. You only pay for employees who are enrolled. If an employee doesn't participate, there's no charge.

No hidden fees.

$29/mo

per employee

Set up your ICHRA plan in minutes.

Licensed benefits specialist for every employee, included.

Audit-ready compliance reports and plan documents.

Employee reimbursement requests and approvals handled in one place.

Employer-to-employee reimbursement payments, automated.

Virtual card for direct premium payments.

Automatic expense classification and partial reimbursements.

Priority + onboarding customer support

Loved by employees and business owners!

SimplyHRA helps businesses offer the best benefits experience possible to their W2 employees.

"I hated having to deal with group plan drama every year. SimplyHRA empowered everyone on my team to manage their own healthcare while I set an annual budget. No more drama! Plus my accountant is happier."

Owner, Small Business

"SimplyHRA has been the easiest way to get setup with ICHRA for myself and my team. I used their benefits specialist to find new healthcare plans and couldn't be happier as an employer and W2 employee."

YC Founder

"We were paying extra with another tool that was really just using a spreadsheet. SimplyHRA makes administering ICHRA easy but the real value to me as an employee is the support I get managing my personal healthcare."

HR Manager, Small Business

"I was nervous about losing my group plan but SimplyHRA's benefits specialist found me one within a week that allows me to keep my doctor while paying less out of pocket. The virtual card pays my premium on auto-pay."

Employee receiving HRA Benefits

ICHRA FAQs

Common questions from employers and employees about how ICHRA works.

How does the virtual card work?

Your employer funds a virtual Visa card each month with their HRA contribution. The card pays your insurance premium directly to your carrier. You can add it to Apple Wallet or Google Pay or enter the card number in your carrier’s payment portal. Simply upload proof of payment into SimplyHRA after you're done.

What if an employee doesn't enroll in health coverage?

Employees must have qualifying individual health coverage (such as a plan from the ACA marketplace or a private insurer) to receive reimbursements. If they don’t enroll in a plan, they won’t be eligible for ICHRA funds. However, your business only reimburses actual expenses, so you never pay for unused benefits.

Can employees who enroll in our ICHRA still take Marketplace premium tax credits?

Generally no. If an employee accepts an ICHRA that’s deemed “affordable,” they are ineligible for premium tax credits for those covered months. If the ICHRA is unaffordable, the employee may decline it and pursue credits on the Marketplace. Affordability compares the employee’s required contribution for the lowest-cost silver plan (self-only), net of the employer allowance, to the IRS affordability threshold.

Are business owners eligible to participate?

C-Corp owners with W2's are eligible. Other business types do not currently qualify for their owners to claim HRA benefits.

When can employees pick plans—can they start mid-month?

Individual health coverage generally starts on the 1st of a month (Marketplace rules). Your ICHRA can start any day but can not cover previous month costs. New hires and qualifying life events trigger special enrollment windows.

Can employees buy any plan they see on the public Marketplace?

Yes—eligible employees can shop and enroll in individual major medical plans on- or off-exchange, subject to enrollment windows. For tax-free reimbursement, the plan must meet Minimum Essential Coverage (MEC).

Does SimplyHRA help employees choose qualified medical, dental, or vision coverage?

Yes. Every employee gets a free, one-on-one call with a licensed benefits specialist who reviews your family size, doctors, prescriptions, and budget to recommend the best plan options. We’re authorized in all 50 states.

How long does onboarding take?

Most employers are fully set up in 2–3 weeks. Employees receive their virtual cards within 3–5 business days after submitting enrollment documents. If you have an urgent hire, we can expedite.

Is the HRA contribution pre-tax or post-tax?

For employers, eligible HRA reimbursements are generally deductible business expenses. For employees, properly substantiated reimbursements are generally tax-free. Any unreimbursed premium amount is normally paid after tax, unless the employer offers a Section 125 cafeteria plan and the employee has eligible off-Exchange individual coverage. Marketplace premiums cannot be paid through Section 125 salary reduction.

Still have questions?

Can’t find the answer you’re looking for? Contact us! We're here to help.

HRA blog, glossary, and more

Resources for employers and employees to learn more about HRA benefits.

Does My Health Plan Qualify for an ICHRA? A Plan-by-Plan Guide

Marketplace, Medicare, COBRA, a spouse's plan — see exactly which health plans qualify for an ICHRA and what to do if yours doesn't.

Read post

SimplyHRA vs Take Command

Compare SimplyHRA and Take Command to find the best ICHRA platform for your business based on pricing, company size, features, and compliance automation.

Read post

Waiting Period

Clear guidance on ACA 90-day waiting periods, ICHRA timing, common mistakes, and best practices for small business compliance and employee communication.

Read post

W-2 Safe Harbor

Understand the W-2 Safe Harbor for ACA affordability: how it works, employer responsibilities, common pitfalls, ICHRA interaction, and compliance tips.

Read post

Ready to Cut Your Benefits Costs and Give Employees Better Coverage?

Schedule a free 15-minute consultation. We’ll walk you through a demo, pricing, the virtual card, and exactly how setup works. No commitment required.

Happier employees with plans they love.

Easy to set up.

Tax-free employer contributions.