Health Insurance Guide for Startups

Think it's too early for your startup to offer employee health benefits?

Think again.

Remember, the startup industry is a brutally competitive landscape.

It's not just a clash of ideas and products — it's also about attracting and retaining the top talent to keep the company thriving.

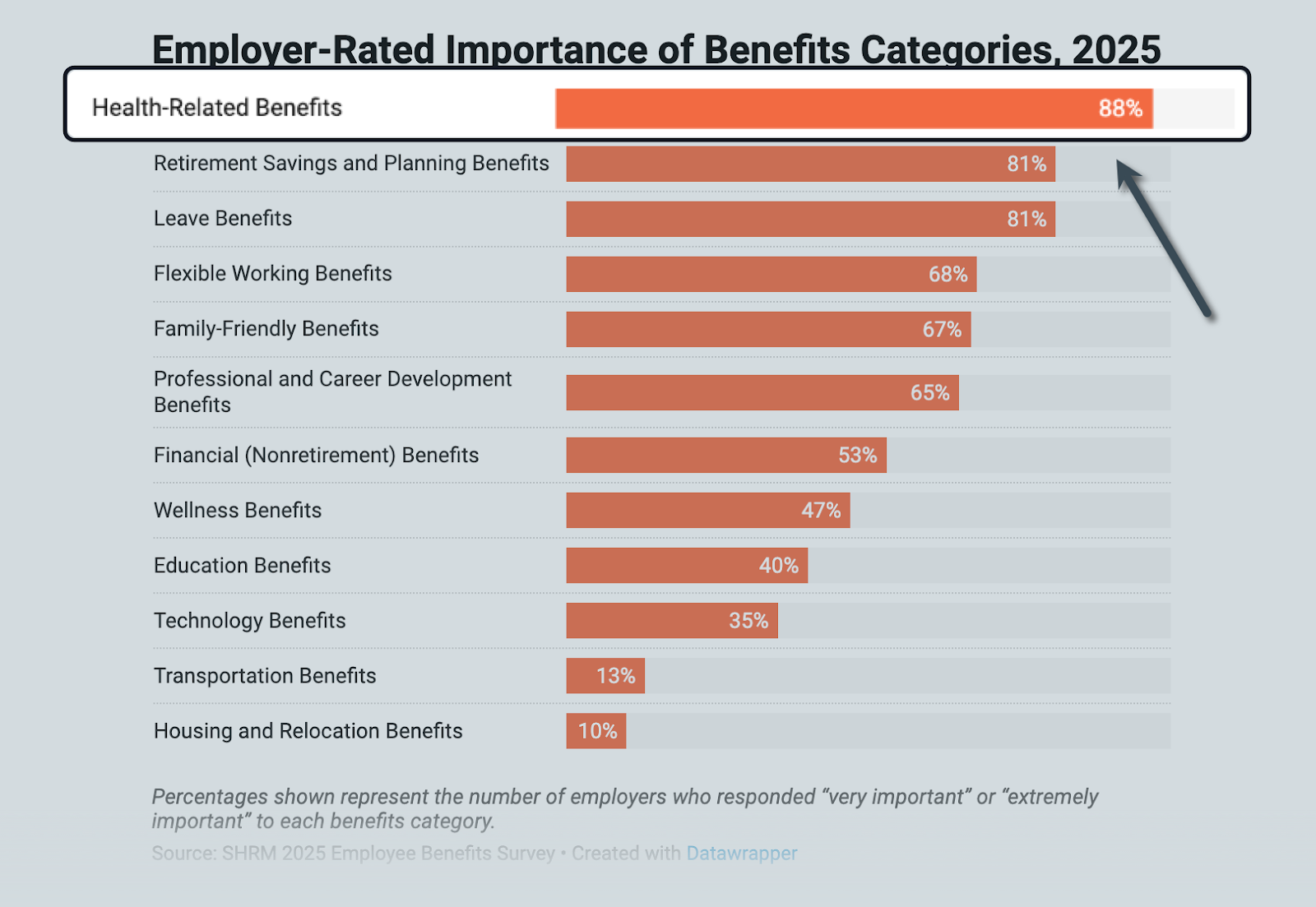

Data from SHRM revealed that 88% of employees consider healthcare-related benefits as "very important" or "extremely important."

In this post, we'll walk you through the nitty-gritty of choosing and rolling out the ideal health insurance plan for your startup.

Let's dive in.

Why Your Startup Needs Health Insurance

Other than attracting talent, below are the top reasons why startup founders should consider offering employee health insurance as early as possible:

- Improve employee retention — According to HSA for America, having a robust health benefits plan for employees reduces turnover by 26%. This will protect you from the costly and disruptive process of backfilling positions.

- Boost employee productivity and well-being — Providing quality healthcare benefits helps keep your team in full strength. Knowing that they're covered also gives employees peace of mind, sharpening their focus and enhancing their productivity.

- Capitalize on tax savings — Startups and small businesses that make less than $50,000 annually can benefit from tax credits, like the Small Business Health Care Tax Credit. They're also eligible to purchase insurance from the Small Business Health Options Program (SHOP) marketplace, leading to long-term savings.

Of course, there's also the legal aspect of providing health benefits to employees.

Health Insurance Options for Startups and Small Businesses

Without further ado, here are 5 of the best health insurance plans for startups and small businesses:

1. Individual Coverage Health Reimbursement Arrangement (ICHRA)

Why Choose ICHRA:

- Predictable costs

- Employee choice

- Flexible

- Portable

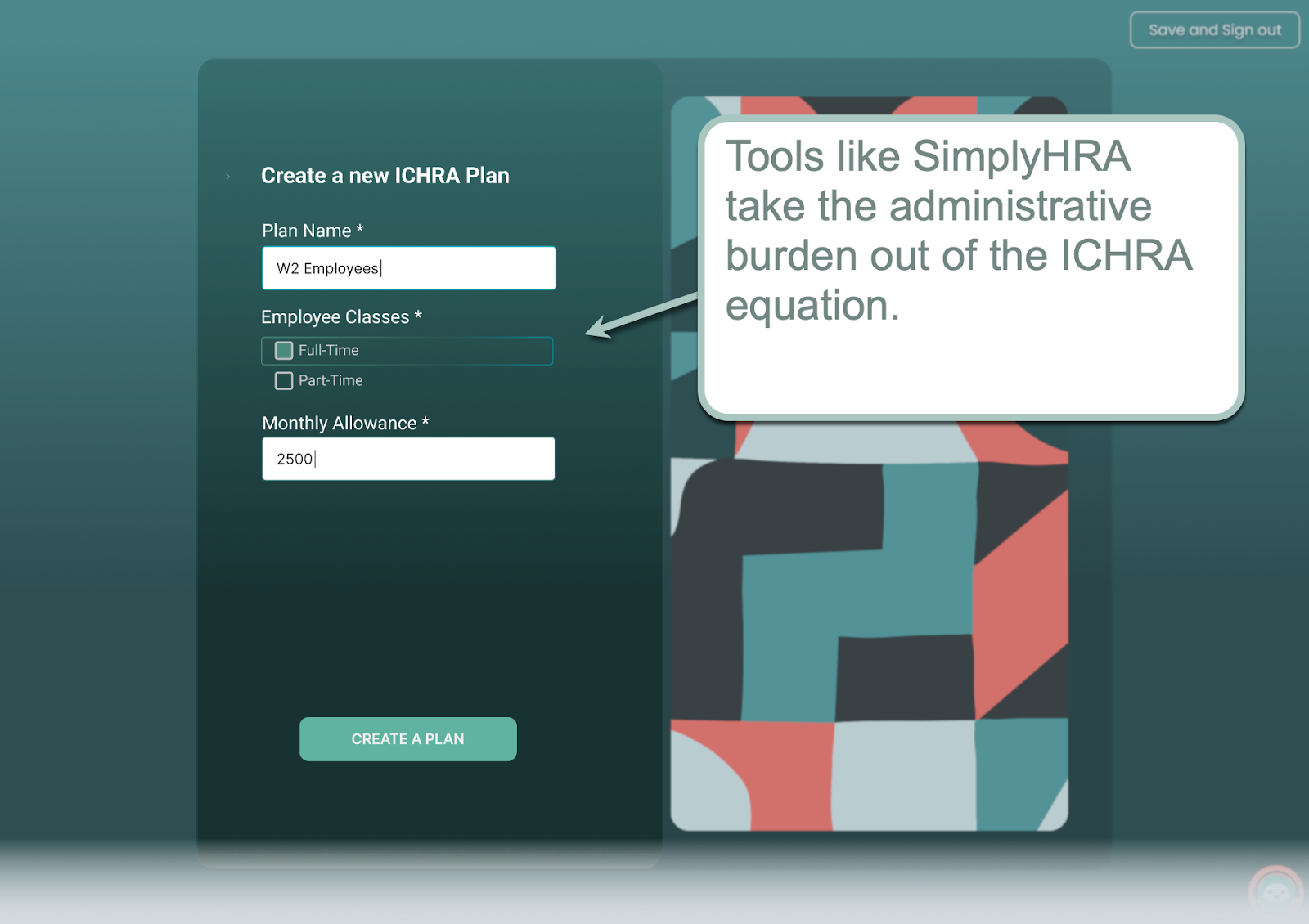

Individual Coverage Health Reimbursement Arrangement (ICHRA) is a type of HRA that allows employers to set a monthly healthcare allowance for each enrolled employee.

At the same time, you're free to specify different employee groups to fine-tune your budget depending on their coverage needs.

As for the actual health insurance plans, ICHRA grants employees the autonomy to choose a product that suits them.

With SimplyHRA, you can breeze through the ICHRA setup process using an intuitive visual interface. Everything from defining employee groups to onboarding members can be done in minutes, while the platform handles all the paperwork and compliance-related tasks in the background.

Schedule a personal demo here.

2. Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

Why Choose QSEHRA:

- Affordability

- Employee choice

- Simplified administration

QSEHRA is another type of HRA that focuses on affordability, but comes with slightly more restrictions.

For one, State the 2026 QSEHRA contribution cap and clarify the employee-count definition; note that QSEHRA applies to fewer than 50 employees and caps differ by family composition and year.

TL;DR, QSEHRA closely resembles ICHRA, but sacrifices some flexibility for lower costs.

3. Fully-Insured Group Health Plans

Why Choose Fully-Insured Group Health Plans:

- Straightforward

- Predictable costs

- Comprehensive coverage

- Risk management

A traditional fully-insured group health plan is implemented through an insurance carrier, which assumes the risk of paying for employee claims.

Although traditional healthcare plans are generally more expensive than HRAs (e.g., ICHRA and QSEHRA), their value proposition includes better risk management for employers and a more robust coverage for employees. It's also worth noting that traditional group plans apply a blanket policy for all enrolled employees.

4. Self-Funded Health Plans

Why Choose Self-Funded Health Plans:

- Flexible

- Offers more control

- Customization

- Scalable

Self-funded plans are exactly what they sound like.

In this plan, the employer shoulders the financial responsibility of paying for qualified insurance claims. They're also in charge of putting together healthcare packages that employees can choose from.

While self-funded plans can be risky, it's a great choice for startups looking for complete control in terms of costs and employee benefits.

5. Professional Employer Organizations (PEOs)

Why Choose PEOs:

- Share risk with other companies

- Streamline HR tasks

- More affordable access to premium insurance products

Lastly, startups can outsource tasks like payroll, compliance, and health insurance from PEOs.

A PEO is a larger group of companies that share healthcare-related financial risks while pooling resources for premium benefits designed for big businesses. PEOs are also often considered HR partners since they handle administrative tasks related to employee management, enabling startups to focus solely on growth.

The drawbacks, however, include less control over policies and potential hidden costs.

Things to Consider When Choosing a Health Insurance Plan

Ready to choose a health insurance plan for your startup?

Remember, offering employee healthcare requires deep, strategic decision-making.

To guide you through the selection process, here are four crucial things to consider:

- Your budget — First and foremost, narrow down your options based on what you can realistically afford, given your company's finances. Use tools like SimplyHRA's cost calculator to assume a more informed position.

- Employee needs — Compile a list of must-have healthcare benefits to ensure you pick a plan that covers them. A workaround, of course, is to go with an HRA like ICHRA to defer the decision to employees.

- Scalability — Are there huge organizational or financial changes on the horizon? Consider the transitional challenges or constraints that an insurance plan presents.

- Administrative overhead — It's also important to think about the administrative burden associated with your desired plans. Do you have the budget and human resources to manage them yourself, or would you rather outsource this to a PEO or managed HRA platform?

Health Insurance for Startups: Frequently Asked Questions

How much does health insurance cost for startups?

Recent data shows that the average annual cost of health insurance is $8,951 for single coverage. This climbs all the way up to $25,572 for family coverage.

Do I need an insurance carrier?

An insurance carrier is a must for certain health insurance types, but can be bypassed for options like self-funded plans. There are also self-service platforms like SimplyHRA that can give you total, seamless control over your company's healthcare.

What's the most cost-effective health insurance plan for startups?

The short answer is it depends. QSEHRA, for example, can get you the lowest costs on paper, but the contribution limitations and maximum employee count could lead to gaps in cost-efficiency in the long run.

Conclusion

Dependable employee healthcare is one of the pillars of a thriving startup.

Not only will it help you grow and maintain employees, but it's also the catalyst to building a tightly-knit, goal-driven, and highly motivated workforce.

Looking for an all-in-one platform for your ICHRA plan?

SimplyHRA is a modern, AI-powered ICHRA management solution that streamlines everything — from plan management to ACA compliance.

Click here to request a personal demo and see it in action.

Related blogs

How to Structure ICHRA Allowances: 2026 Compliance Rules

Minimum Essential Coverage (MEC) Definition: 2026 Guide