How Tighter ACA Marketplace Requirements Can Impact Small Business Healthcare

With the One Big Beautiful Bill Act of 2025 signed into law, businesses have had their hands full adapting to the changes.

Employee healthcare, in particular, undergoes a number of headache-inducing shifts — from Medicaid cuts to more frequent reverifications. These changes disproportionately affect small businesses that need to make every dollar count.

One such change is the tighter eligibility requirements for the Affordable Care Act (ACA) Marketplace subsidies. And with over 24 million enrollees relying on Marketplace coverage, to say that the OBBBA is making people nervous is an understatement.

But how exactly does the OBBBA affect the ACA Marketplace?

That's the question, and this post has the answer.

Read on to learn more about the ACA, the OBBBA, and how small businesses can make the best out of them.

What is the ACA Marketplace?

Ever since the ACA (AKA "Obamacare") was signed into law in 2010, the ACA Marketplace has provided businesses and individuals with reliable healthcare coverage — without breaking the bank.

Each state comes with its own health insurance exchange marketplace, ensuring healthcare prices stay in line with the local economy.

For small businesses, the Health Insurance Marketplace came with the Small Business Health Options Program (SHOP). This allowed employers with 50 or fewer Full-Time-Equivalent (FTE) employees to purchase cost-effective group health and dental insurance.

In addition, the ACA Marketplace unlocked a number of other benefits for growing businesses:

- Tax advantages — Small businesses paying for health insurance through SHOP are eligible for tax credits up to 50% of premium costs.

- Streamlined ACA compliance — Purchasing employee health insurance from the ACA Marketplace pretty much guarantees compliance right out of the box.

- Caters to different employee classes — ACA Marketplace plans come in four categories (Bronze, Silver, Gold, and Platinum) to fit different needs and budgets.

- Affordable coverage for low-risk individuals — The ACA also offers a "Catastrophic" plan for enrollees under the age of 30 (or those qualifying for a hardship or affordability exemption), coming with very low premiums but high deductibles.

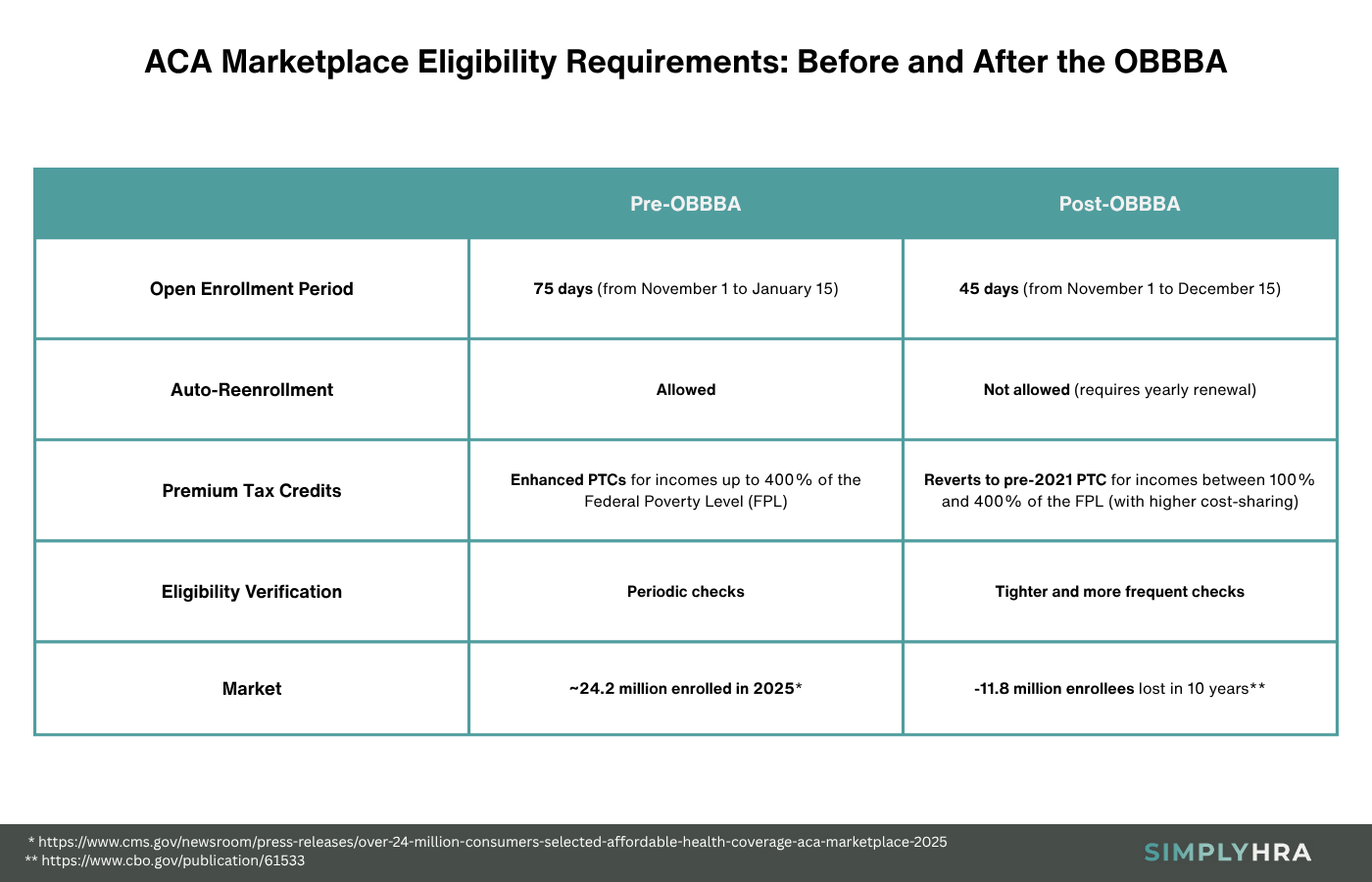

While the ACA provided millions of Americans with reliable coverage, the Congressional Budget Office (CBO) projects that around 11.8 million people could lose their benefits over the next decade since the OBBBA's signing.

Yes, that includes ACA Marketplace customers.

These losses will primarily stem from stricter eligibility and pre-verification requirements, which brings us to the healthcare provisions in the OBBBA.

How the OBBBA Tightened ACA Marketplace Requirements

First and foremost, remember that the impact of the OBBBA on healthcare is multi-faceted. This includes Medicaid spending cuts, more frequent eligibility checks, and — of course — tighter ACA Marketplace requirements.

Here's a more detailed breakdown:

- Automatic reenrollment — With the OBBBA in place, all auto-reenrollment processes are canceled, requiring all enrollees to actively renew their coverage each year.

- Verification procedures — Verification of immigration status, citizenship, and income is stricter and more frequent (with zero flexibility for non-legal or undocumented immigrants).

While these provisions reflect the direct changes caused by the OBBBA, some agencies like the CBO anticipate indirect changes to the ACA ecosystem due to the new bill.

For example, tighter eligibility requirements can reduce the number of ACA planholders by the millions. This reduces the risk pool (increasing concentration of higher-risk individuals), resulting in lower insurer participation and potentially higher average cost of premiums.

What it Means for Small Businesses

How will the changes in the ACA Marketplace affect small businesses?

Below are the direct implications of the post-OBBBA ACA Marketplace economy to the small business world:

- Increased administrative burden and costs — Companies that offer group insurance will be forced to take on a more active role in maintaining their employees' coverage. This is due to the elimination of auto-reenrollment and shortened reverification windows.

- Higher premium costs — The OBBBA causes a ripple effect that reduces insurer participation as well as the risk pool, which leads to lower profitability for insurers. This will likely lead to higher premium costs and increased volatility.

- Fewer coverage options — With carriers pulling out of the Health Insurance Marketplace, employers and employees will have fewer plans to choose from. Keep in mind that this includes SHOP plans, which are a core reason why small businesses choose to buy insurance from the Marketplace.

On the flip side, the OBBBA does include changes that can boost the appeal of ACA Marketplace plans.

For one, the OBBBA now allows individuals enrolled in Bronze and Catastrophic plans to open and contribute to a Health Savings Account (HSA). This provides individuals with long-term peace of mind, knowing that they can save pre-tax dollars for future healthcare costs.

The question now is, how can companies reap the benefits of the expanded HSA eligibility while adapting to rising costs and administrative overhead?

Why You Should Consider ICHRA in the Post-OBBBA World

Add: 'Each participating employee must be enrolled in individual health insurance coverage (on- or off-Exchange) or Medicare; ICHRA alone does not satisfy the group health plan requirement.' Employees are then free to choose their preferred individual health insurance product, allowing employers to focus on more meaningful aspects of running their business.

Revise: 'ICHRA contributions are set by employer discretion, but must be reasonable and meet affordability standards under IRC §4980H for each class of employees.' It's also double-tax-advantaged with tax-deductible contributions and tax-free reimbursements.

Why ICHRAs Make Sense Post-OBBBA

Aside from the fundamental advantages of ICHRA, here's how it can offer the best case scenario for small businesses as far as post-OBBBA healthcare goes:

- Clarify: 'An affordable ICHRA renders employees ineligible for PTC; they use the fixed employer allowance instead. If ICHRA is unaffordable, employees may decline and seek PTC, and will handle their own verification for PTC purposes.'

- Offset rising costs and volatility — With ICHRA, companies are able to set fixed reimbursement allowances that will be unchanged regardless of external market factors.

- High flexibility — ICHRA not only allows employees to choose an individual healthcare plan tailored to their specific needs, it's also compatible with other instruments like Direct Primary Care (DPC) arrangements and HSAs.

The drawback is, companies need to pour resources into employee training and guidance to build an effective ICHRA plan.

Leaving employees in the dark — burdened to handle everything themselves — can be a huge blow to employee satisfaction.

Fortunately, there are solutions that can streamline every component of your ICHRA plan.

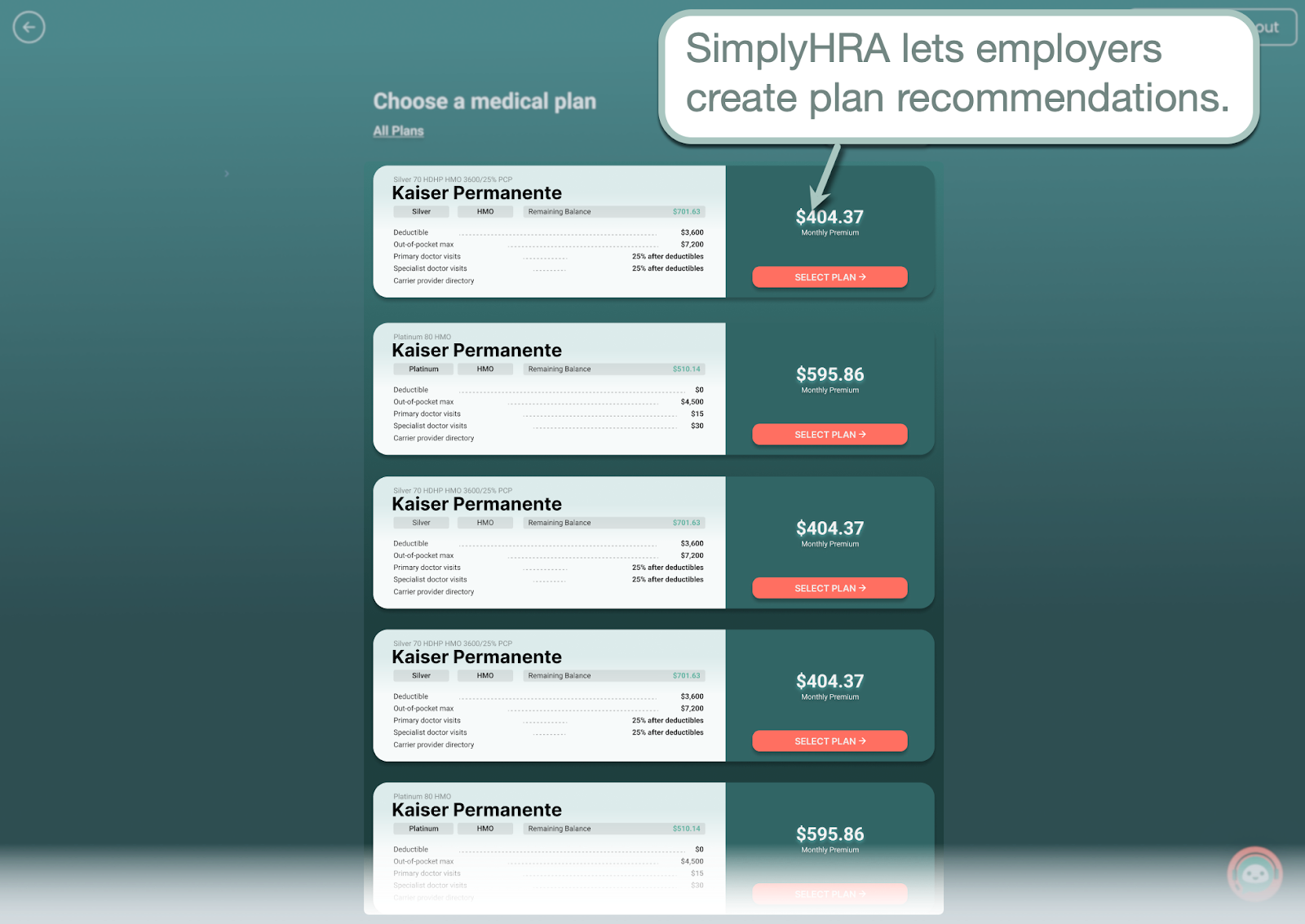

Self-service platforms like SimplyHRA, for instance, allow employers to set recommended plans to expedite the enrollment process.

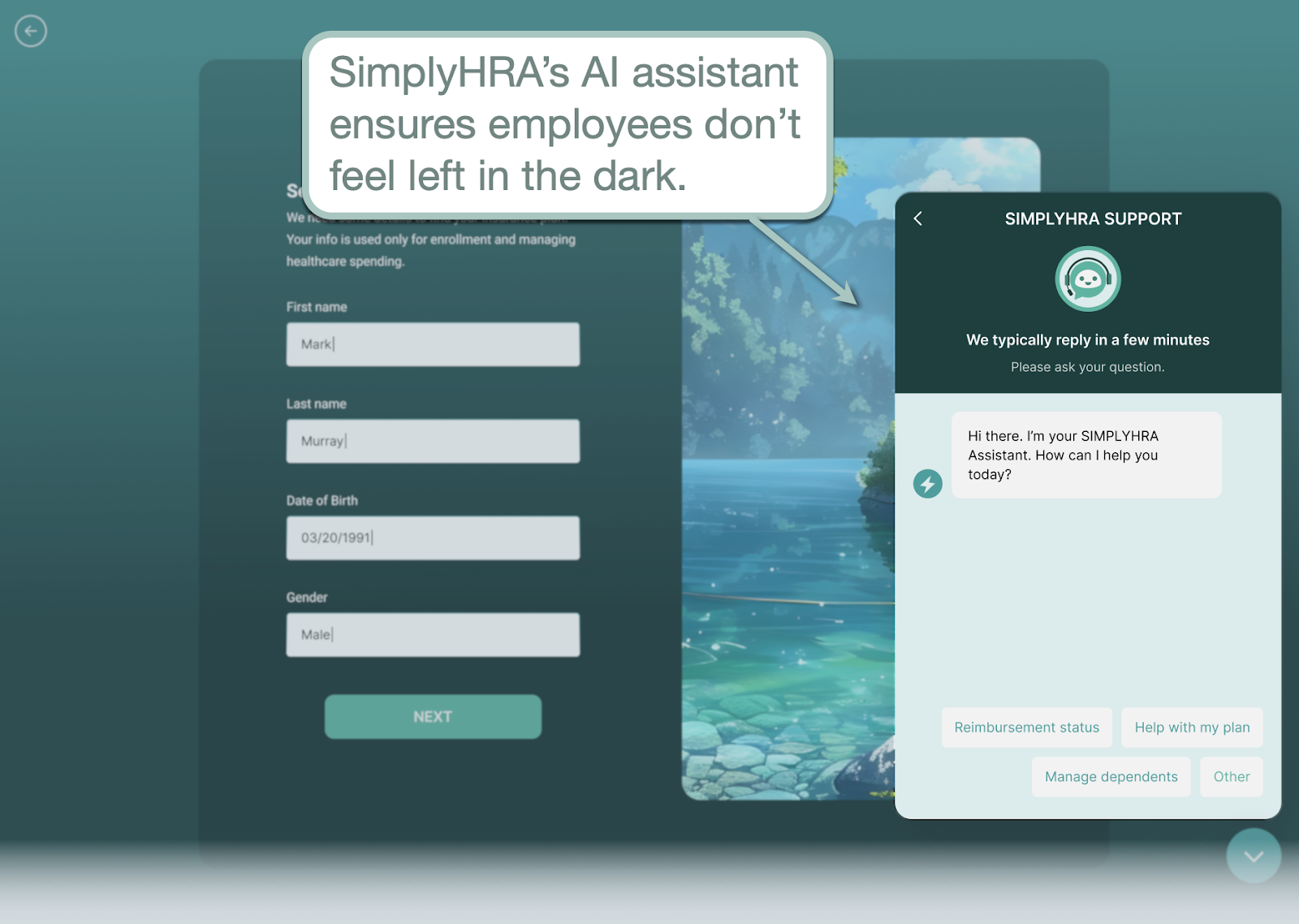

For on-demand assistance, SimplyHRA is also equipped with an AI assistant — ready to be of service to employees at a moment's notice. Employees can follow up on reimbursement requests, get assistance during setup, and find answers to healthcare-related questions without picking up the phone or even leaving the app.

Finally, SimplyHRA also makes the setup and management facets of ICHRA incredibly easy.

Using the visual interface, weeks of preparation can be condensed into a few hours of setup — no need to hire a third-party insurer, broker, or expert. The SimplyHRA team also ensures all paperwork related to compliance and reporting is handled with minimal intervention.

Conclusion

While the tighter ACA Marketplace requirements can be a significant roadblock, there's always a way for small businesses to adapt and thrive as long as they have the proper tools.

Building a lean ICHRA plan with SimplyHRA, for example, is a great workaround to the post-OBBBA challenges while providing employees with the flexibility and peace of mind they deserve.

Book a personalized demo here to get a closer look at SimplyHRA's features.

Related blogs

Should I Buy a Pre-Funded ICHRA Debit Card? 2026 Guide

How Employees Reconcile APTC After Joining Employer HRA 2026