How the One Big Beautiful Bill Impacts HSAs

The One Big Beautiful Bill Act (OBBBA) of 2025 is a sweeping piece of legislation that affects nearly every aspect of running a small business.

When it comes to small business health insurance, the changes can be summed up into tighter regulations, Medicaid cuts, and a few silver linings that businesses can cling to for relief amidst the turbulence.

One such benefit would be the expanded eligibility for Health Savings Accounts (HSAs), which benefits over 70 million Americans.

This begs the question: How do you take the upsides out of post-OBBBA healthcare while leaving all the bad stuff behind?

Individual Converage Health Reimbursement Arrangements (ICHRAs) just might be the perfect answer.

In this post, we'll discuss why an ICHRA plan offers a great alternative to traditional group health plans and Professional Employer Organization (PEO) coverage, especially in the post-OBBBA landscape with the expanded HSA eligibility.

But first, a quick word on HSAs.

What is an HSA?

An HSA is basically a tax-advantaged savings account for those covered by a High-Deductible Health Plan (HDHP).

The basic mechanics of HSAs are simple.

If an employee has an HDHP, they (or their employers) can put money into an HSA account, which can be withdrawn to cover qualified medical expenses like prescription medication, dental care, doctor visits, and mental health services.

The idea is to have a reliable source of funds that can rollover indefinitely and be ported over in case the individual moves to a new employer. HSAs are also "triple-tax-advantaged" with the following benefits:

- Contributions to HSAs are considered tax-deductible

- HSA interest earnings are non-taxable

- Withdrawals for qualified expenses are tax-free

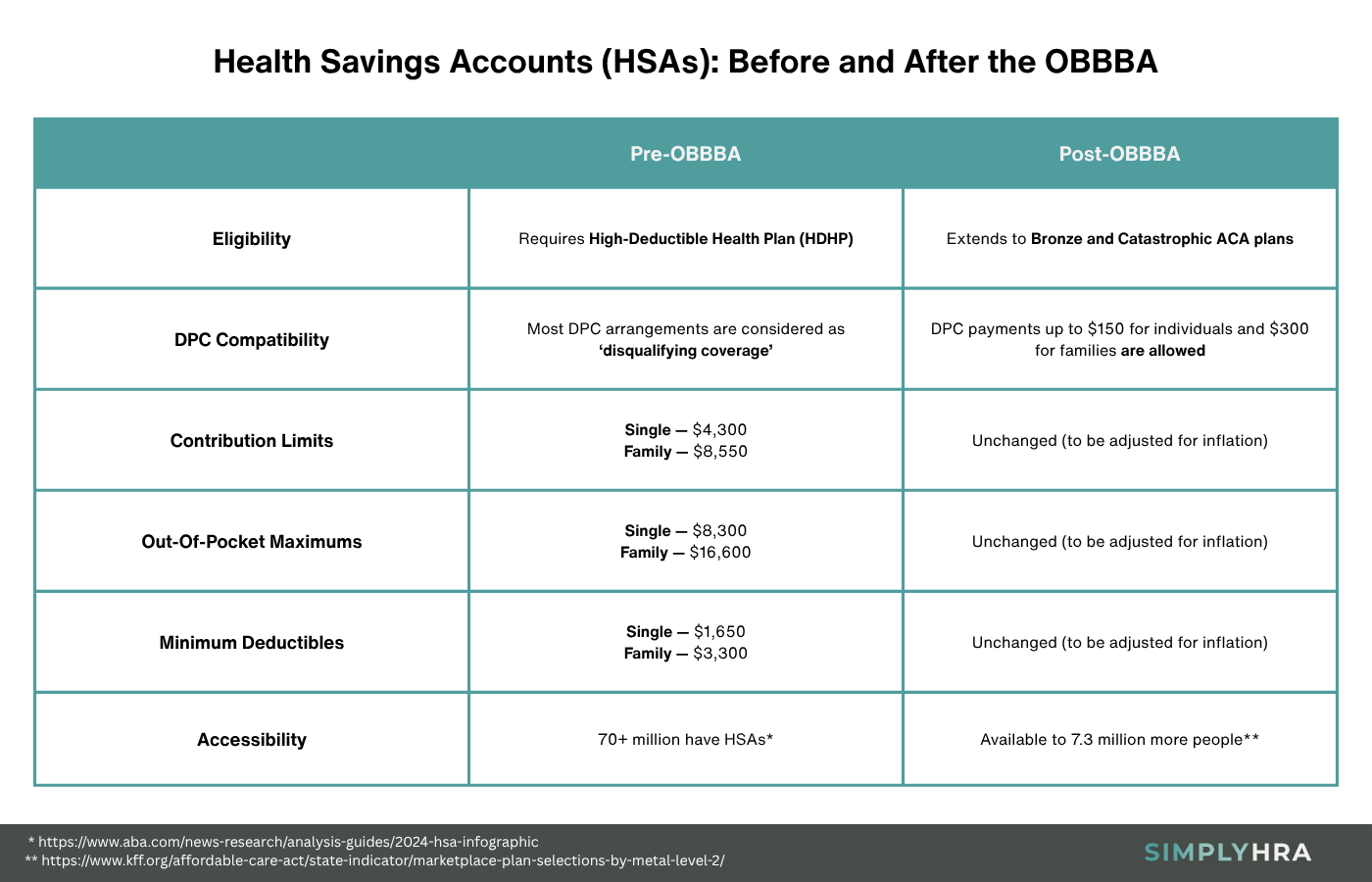

For 2026, HSAs have an annual contribution limit of $4,400 for individuals and $8,750 for family coverage (per IRS Rev. Proc. 2025-19).

Another benefit of HSAs is that they can be transferred to a spouse or dependent upon the account holder's death.

Transfers to a surviving spouse are non-taxable and can continue to function as an HSA — only under a different name. However, transfers to a non-spouse dependent are given as a lump sum, which is subject to income tax and can no longer be reinstated as HSAs.

With all these advantages, how come not everyone has an HSA in their healthcare plan?

The thing is, an HSA traditionally came with a few restrictions that made it incompatible with a lot of coverage options.

Here's a brief rundown of these restrictions:

- HDHP requirement — To use an HSA, employees need to be enrolled in an HDHP, which is characterized by a minimum deductible of $1,700 for individual and $3,400 for family coverage. HDHPs were also defined to have out-of-pocket maximums of $8,500 for individuals and $17,000 for families (per IRS Rev. Proc. 2025-19, applicable to plan years beginning in 2026).

- Direct Primary Care (DPC) conflict — In the context of HSAs, DPCs are in a gray area that would often disqualify individuals for eligibility. While it can be done through extremely careful documentation, the Internal Revenue Service (IRS) traditionally viewed DPC payments as disqualifying health coverage.

- Inaccessible to enrollees with bronze and catastrophic plans — Another significant roadblock to the adoption of HSAs would be their incompatibility with bronze and catastrophic plans. These plans can be purchased through the Affordable Care Act (ACA) Marketplace, covering around 31% of customers.

These restrictions by themselves make HSA eligibility a huge challenge for a substantial chunk of the American workforce. This includes low-income earners with bronze plans and younger individuals with catastrophic plans — as well as workers with DPC arrangements for specific healthcare needs.

But with the OBBBA signed into law, more people will be able to integrate HSAs into their healthcare plans.

Workers enrolled in bronze and catastrophic ACA plans are now eligible to open HSAs. The same goes for those under DPC arrangements up to $150 per month for individuals and $300 for families.

Here's a side-by-side comparison:

All things considered, having an HSA provides employees with long-term peace of mind. And with the OBBBA projected to cut Medicaid spending by $1.09 trillion over the next decade, there are bound to be businesses transitioning over to HSA-eligible plans in the near future.

Unfortunately, shifting employee healthcare solutions is easier said than done, especially for small businesses with limited human resources.

You need to contend with a series of administrative hurdles, like plan selection, compliance, employee coordination, and DPC integration.

If only there were a better alternative that minimizes these headaches.

This is where ICHRA comes in.

What is ICHRA?

ICHRA is a form of HRA where employers provide a monthly allowance to cover health insurance premiums and other eligible medical expenses.

Here are some of the top reasons why ICHRA is perfect for HSAs in the post-OBBBA world:

- No contribution limits — ICHRA has no minimum and maximum contribution limits. This uncomplicates the process of structuring a plan that accommodates HSAs.

- Tax advantages — ICHRA plans are also tax-advantaged with tax-free reimbursements and tax-deductible contributions. This also applies to DPC payments, which complement the OBBBA's expanded eligibility provisions for HSAs nicely.

- Reduced administrative burdens — ICHRA enables employees to choose and purchase their own insurance products. In exchange for this autonomy, employees are also required to handle enrollment-related tasks.

- Compatibility with DPC arrangements — The OBBBA's provisions in regard to DPC payments make them predictable. This is perfect for crafting ICHRA plans that cater to your employees' specific healthcare needs.

Aside from these benefits, implementing an ICHRA plan for your small businesses can also be done in two easy ways.

First, you can expedite the process by outsourcing a third-party platform to set up and manage your plan. In exchange for a flat annual or per-employee monthly fee, you get speedy and hassle-free ICHRA administration.

A more cost-effective alternative, however, is to use an intuitive, self-service ICHRA management product like SimplyHRA.

Setting Up Your ICHRA Plan with SimplyHRA

With the help of SimplyHRA, all setup and administrative tasks related to your ICHRA plan can be done in one dashboard.

Here's an overview of the setup process:

- Step 1: Sign up with your email or by linking your Google account. Complete your registration by entering important business details like your EIN, company name, number of employees, and business type.

- Step 2: Build your ICHRA plan by specifying the employee class it's for (full-time or part-time), setting a monthly allowance, and giving it a name. Make sure it's enough to cover the costs of your employees' healthcare needs, including DPC payments, HSA contributions, and health insurance.

- Step 3: Add your employees by filling in their details, including their employment type and contact information. Onboarded employees will then be able to submit their own eligible plan, choose from your pre-set plans, submit documents, and apply reimbursements through their employee portal.

- Step 4: That's it — you can now start handling reimbursement requests and tracking your ICHRA budgets from within SimplyHRA. The solution takes care of compliance so you can focus on managing payroll deductions, reimbursements, and your balances.

Remember, everything concerning your ICHRA healthcare plan is done through your SimplyHRA dashboard.

There's no need to hire a third-party administrator or retool your payroll systems. SimplyHRA is a turnkey solution that has everything you need to get your ICHRA plan up and running in no time.

Other Features of SimplyHRA

Below are other reasons to manage your ICHRA plan with SimplyHRA:

- Mobile app version — You and your employees can use the SimplyHRA mobile app to access all features. No need to drop what you're doing and get to your work computer to approve urgent reimbursement requests, onboard new employees, and so on.

- Set up your payment system — Link your bank account for automated reimbursement contributions. Employees, on the other hand, can use their virtual card (or order a physical card) to cash out reimbursements.

- Assisted employee onboarding — The SimplyHRA interface contains intuitive elements that require little to no training. For example, upon signing up, employees can use a slider to set their desired out-of-pocket maximums to get personalized plan recommendations.

- SimplyHRA AI assistant — Finally, employers and employees alike can utilize the built-in AI chatbot whenever they need assistance. They can ask questions, follow up on reimbursement requests, add dependents, verify eligible expenses, and more.

Conclusion

There's no question that we're in for a very interesting time now that the OBBBA is signed into law.

The expanded HSA eligibility, tighter ACA marketplace requirements, and slimmer Medicaid funding — all indicators point to a need for small businesses to re-evaluate their employee health benefits strategy.

With ICHRA, you can take advantage of the positive changes that the OBBBA brought while circumventing the inconveniences in terms of restrictions and affordability. And the best way to move forward is to look for a cost-effective, all-in-one solution like SimplyHRA.

Related blogs

Should I Buy a Pre-Funded ICHRA Debit Card? 2026 Guide

How Employees Reconcile APTC After Joining Employer HRA 2026