How the Big, Beautiful Bill Changes Health Insurance for Small Business Owners

Offering quality healthcare benefits is a must-have for businesses looking to maintain a healthy and motivated workforce.

For the past decade, the choices for small businesses boiled down to a handful of health insurance options, like:

- Group health plans

- Professional Employer Organizations (PEOs)

- Health Reimbursement Arrangements (HRAs)

- Self-funded plans

However, the One Big Beautiful Bill Act (OBBBA) of 2025 reshaped the small-business health insurance landscape.

In this post, we'll take an in-depth look at the healthcare provisions inside the OBBBA — from Medicaid cuts to stricter Affordable Care Act (ACA) Marketplace — and how small businesses can navigate this new landscape.

Let's get started.

Health Insurance Provisions in the OBBBA

Before we go any further, here's a breakdown of the healthcare provisions in the OBBBA that affect employers of all sizes:

1. Tighter Affordable Care Act (ACA) Marketplace Eligibility Requirements

With the OBBBA enforced, both employees and employers now face stricter eligibility requirements for premium tax credits. The bill also eliminates provisional eligibility, meaning applicants must pay their full premiums while the Marketplace verifies their information.

Enrollment periods are also shortened by exactly one month — starting from November 1st and now ending by December 15th (from January 15th). Any special, income-based enrollment windows are also written off.

2. Medicaid Spending Cuts and Restrictions

In an effort to reduce spending, the OBBBA is projected to cut Medicaid funding by $1.02 trillion over the next 10 years — a big blow to hospitals across the country that cater to Medicaid patients.

Furthermore, the OBBBA requires individual applicants to complete 80 hours of "qualifying activities" per month for eligibility (for childless adults with no disabilities). This includes:

- Paid work

- Education and training

- Volunteer work

The bill also bans Medicaid funding for Planned Parenthood, encompassing services such as contraception, cancer screenings, and treatment for Sexually Transmitted Infections (STIs). This, of course, is worrisome for workers who rely on Medicaid funding for these services.

3. More Frequent Reverification

Aside from reduced funding, the OBBBA also aims to reduce Medicaid spending by increasing the frequency of eligibility checks.

Prior to the bill, enrollees only needed to undergo reverification every year (or less frequently). After the reforms, eligibility checks must be conducted every six months — coaxing employees to seek alternatives such as employer-funded healthcare.

4. Expanded Eligibility for Health Savings Accounts (HSAs)

Employees covered by High-Deductible Health Plans (HDHPs) are able to put money into tax-advantaged Health Savings Accounts (HSAs), but it traditionally came with a few restrictions.

A big one would be "disqualifying coverage," which pertains to enrollment in certain employer-sponsored plans, Medicare, and other non-HDHP benefits.

The new bill loosens these restrictions to make HSAs more accessible to a wider range of employees. It also institutes permanent first-dollar telehealth coverage for HDHPs with HSAs, which makes remote care accessible before their deductibles are met.

5. Rural Health Transformation Program

The OBBBA includes a provision for the Rural Health Transformation Fund — a $50 billion fund aimed at improving healthcare accessibility and hospital solvency across rural areas. This can potentially reduce costs and offset the negative impact of the Medicaid coverage losses and stricter Marketplace requirements.

To participate in the program, states must seek the approval of the Centers for Medicare and Medicaid Services (CMS) by submitting a plan that outlines:

- How it will improve the healthcare of rural residents.

- Ways it improves access to rural hospitals and healthcare providers.

- New and emerging technologies that will be utilized to empower preventive care and disease management.

- Strategies to improve hospital solvency in rural areas.

These plans had to be approved or denied by the CMS by December 31, 2025.

After which, half of the rural health fund ($25 billion) will be evenly distributed among all approved states from 2026 to 2030. The remaining half, on the other hand, will be distributed by the CMS administrator based on the rural population, existing health facilities, and the status of disproportionate share hospitals in the area.

Despite these changes, the OBBBA preserves a few things for small businesses and startups that may have built their health insurance strategies around them.

For example, the bill preserves tax exclusions for employer-funded healthcare.

Contributions to Individual Coverage Health Reimbursement Arrangement (ICHRA) plans, for instance, remain tax-deductible. This makes ICHRA, along with similar HRAs like Qualified Small Employer Health Reimbursement Arrangement (QSEHRA), a more attractive option for startups and small businesses that need cost-effective healthcare solutions.

While post-OBBBA healthcare may look bleak at first, it also opens up opportunities to reinvent and streamline employee healthcare.

Strategies to Remodel Your Small Business Health Insurance for the OBBBA

There's no question that the OBBBA presents numerous challenges for small businesses and startups, especially when it comes to providing comprehensive healthcare for their employees.

But there's a silver lining behind this cloud.

By adopting ICHRA as the primary healthcare option for your workforce, you can easily circumvent the hurdles associated with the increased compliance demands and potential costs brought by the OBBBA.

What is ICHRA?

ICHRA is a type of employer-funded healthcare plan in which the company sets a monthly reimbursement allowance for each employee group. Employees are then given the freedom to purchase their own individual health insurance and other eligible medical expenses as defined by the employer — 100% tax-free.

Here's how ICHRA can solve your company's healthcare-related uncertainties in the post-OBBBA world:

- Complete cost control — Right off the bat, the amount of control and flexibility that ICHRA brings to the table effectively offsets potential Medicaid coverage losses and rising ACA Marketplace premiums. There are no minimum or maximum limits to the monthly contributions, giving you total control over your employee healthcare budget.

- HSA eligibility of Bronze and Catastrophic ACA plans — ICHRA-covered employees can also contribute to an HSA if they're also enrolled in an HDHP. The expanded eligibility for HSAs under the OBBBA (including Bronze and Catastrophic plans) may lead to increased adoption of ICHRA, as long as they don't have any type of disqualifying coverage.

- Reduced administrative burdens — By letting employees choose their own health insurance, you're freed from some of the administrative and compliance burdens exacerbated by the OBBBA. Instead, your focus should be shifted towards providing adequate training and resources, helping employees make informed decisions when it comes to their healthcare.

In addition to these benefits, ICHRA also veers you away from Medicaid, which has become one of the least appealing healthcare options after the OBBBA was signed into law.

However, implementing an effective ICHRA plan requires a robust platform that streamlines the process.

Managing Your ICHRA Plan with SimplyHRA

SimplyHRA is a comprehensive, AI-powered platform that will help you manage every aspect of your ICHRA plan through a visual interface.

Here's a crash course on how to get set up:

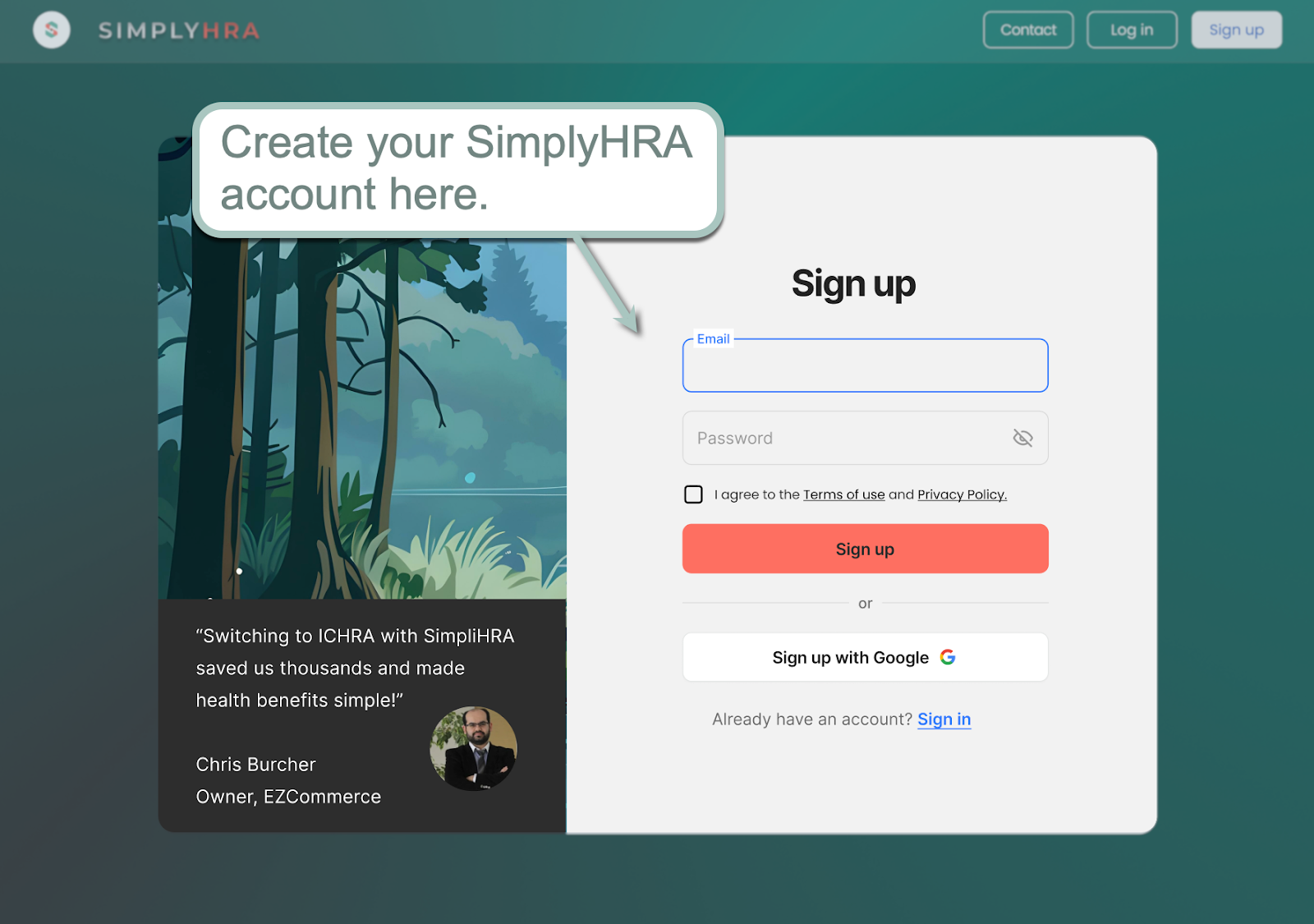

1. Create Your Account

Sign up by entering your desired email and password or by linking your Google account.

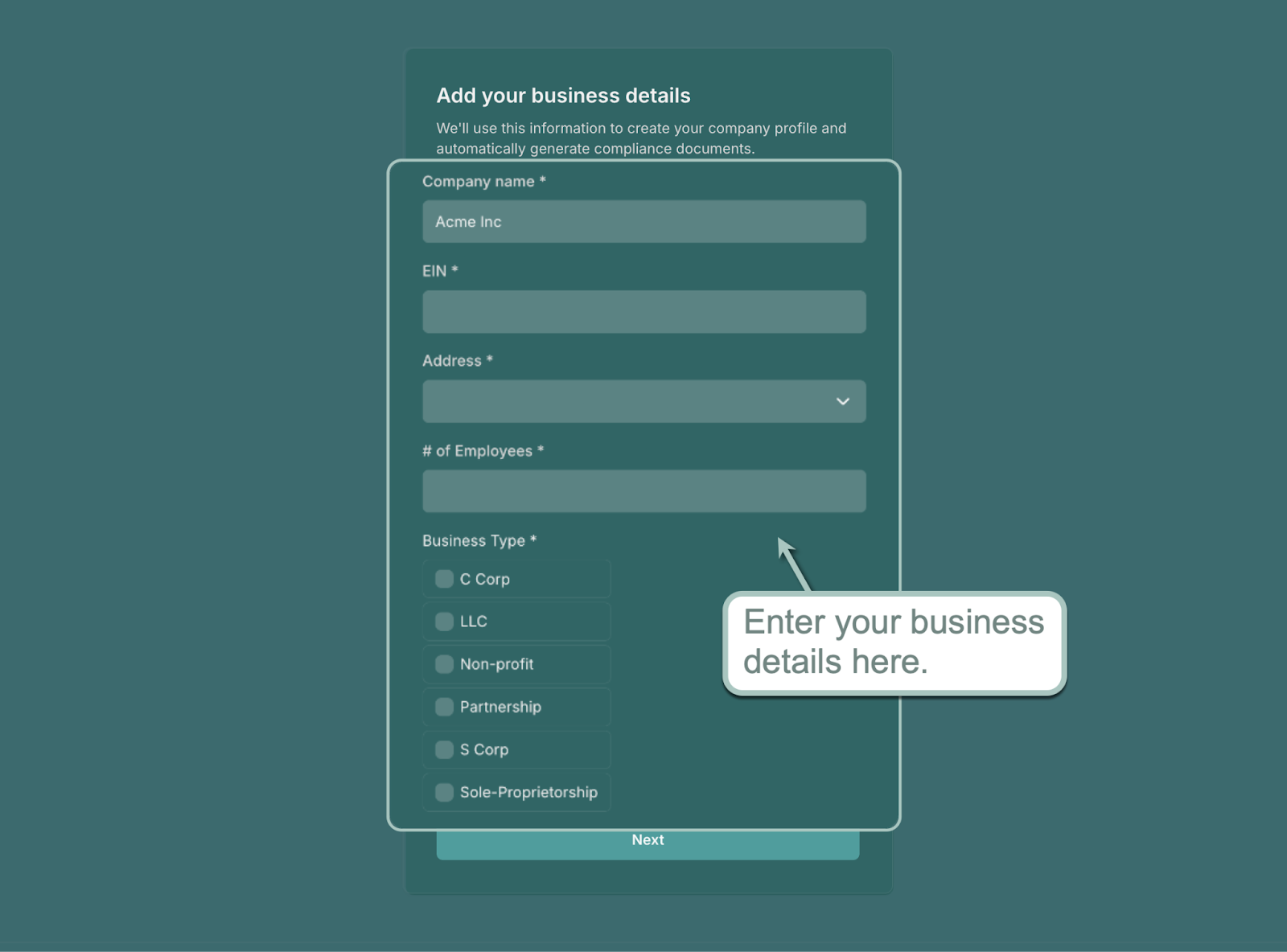

Complete your account by entering your essential business information, such as your company name, EIN, and business type.

2. Configure Your ICHRA Plan

After creating your account, you're ready to set up your first ICHRA plan with SimplyHRA.

The process only consists of three steps: entering your plan's name, picking an employee class (full-time or part-time), and setting a monthly allowance.

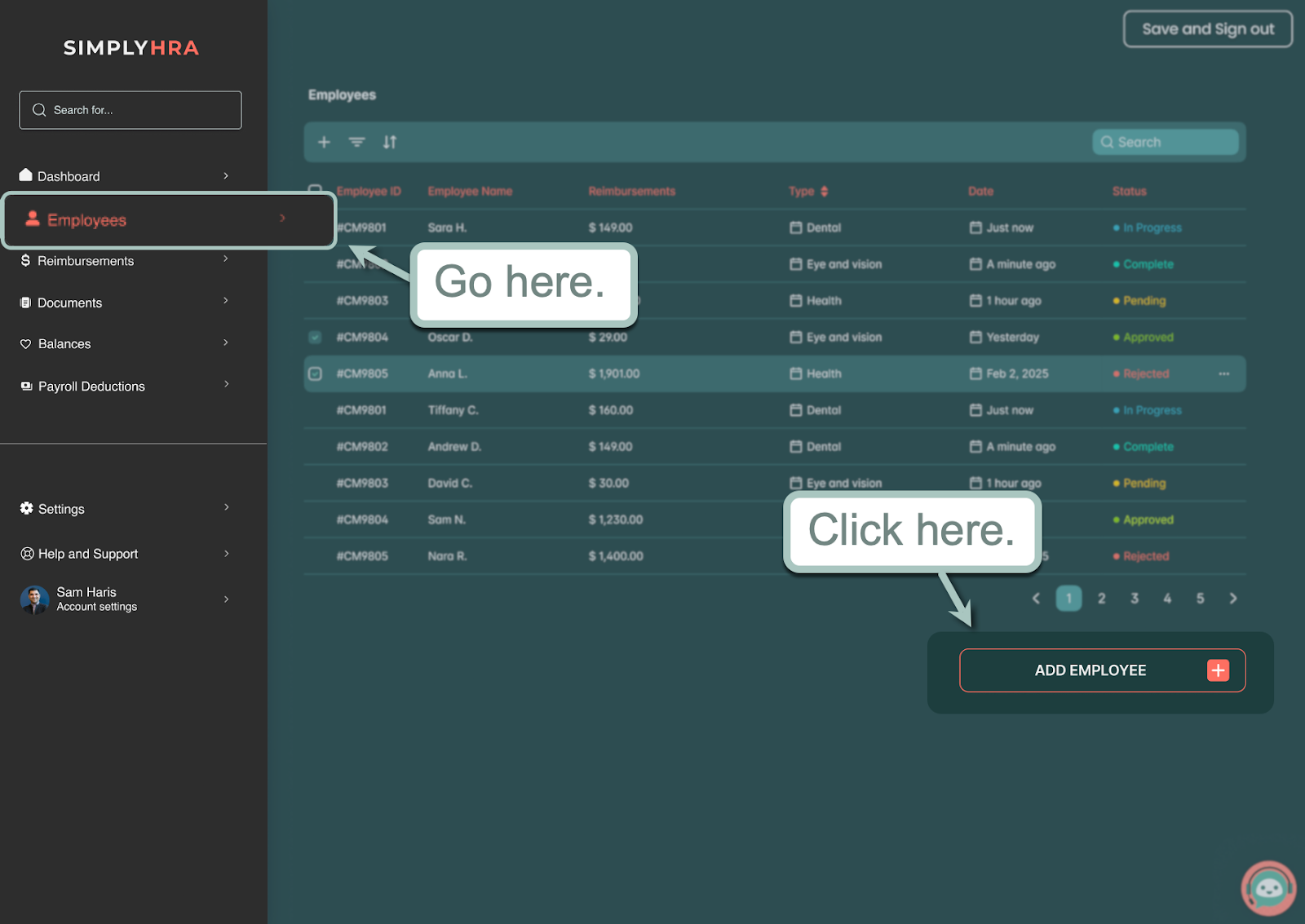

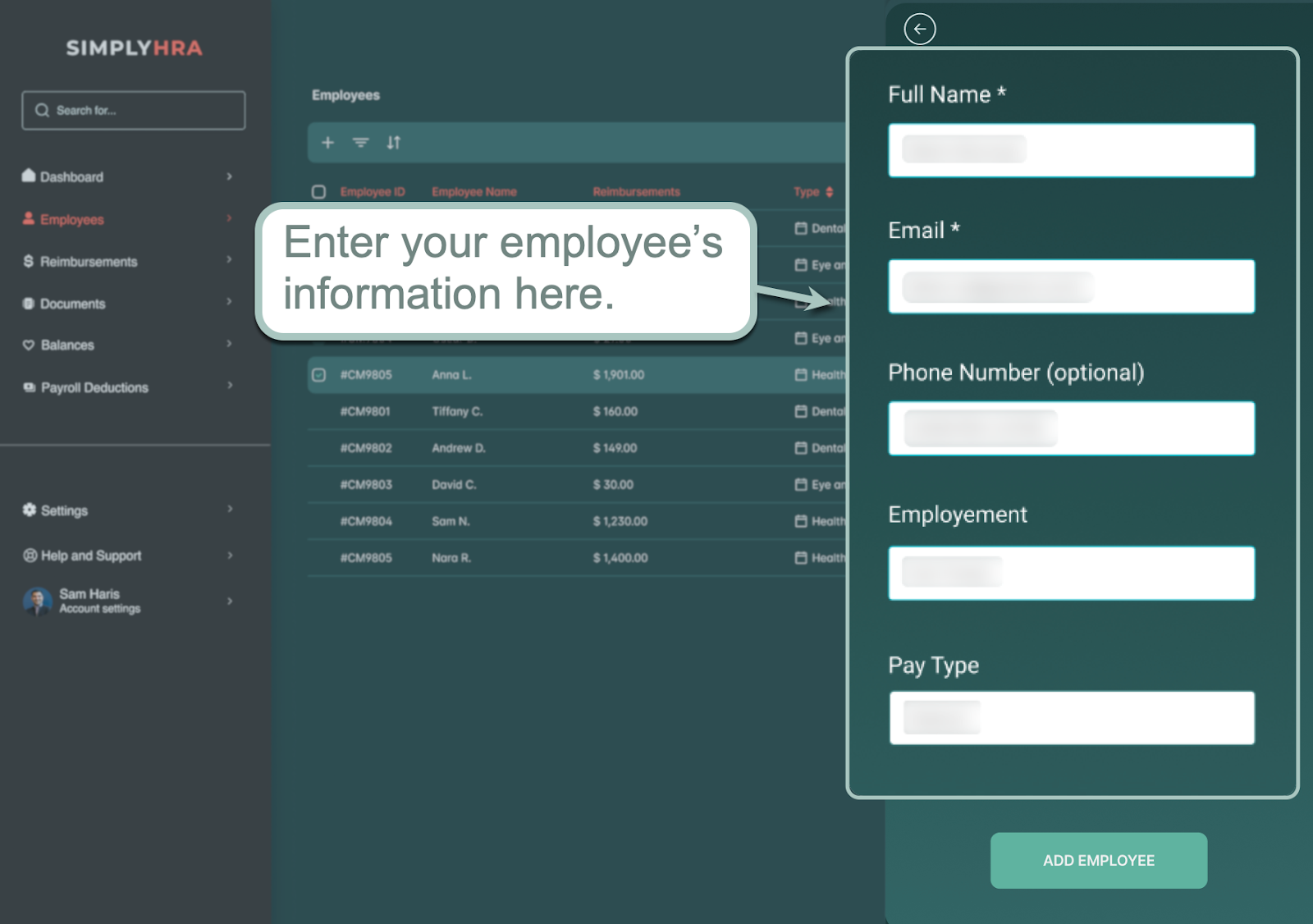

3. Adding Employees

Once your ICHRA plan is ready, it's time to start adding employees.

From the main dashboard, go to the 'Employees' menu and click 'Add Employee.'

Finish adding your employee to the system by entering their full name, email address, pay type, phone number, and employment type. Click 'Add Employee' to lock in their details.

That's it — your ICHRA plan is now up and running.

Aside from setting up your ICHRA plan, here are other benefits of using SimplyHRA for your company's healthcare needs:

- Easy compliance — SimplyHRA handles all paperwork in the background, allowing you to focus on creating tailored ICHRA plans, managing enrollees, and handling payouts.

- On-demand, 24/7 support — SimplyHRA is equipped with an AI assistant that can answer both employee and employer questions, such as reimbursement status queries, troubleshooting, and so on.

- Built-in analytics — Stay on top of your healthcare budgets, reimbursements, and billing dates inside the consolidated SimplyHRA dashboard.

Conclusion

The One Big Beautiful Bill Act of 2025 is a mixed bag of challenges and opportunities for startups and small businesses.

It's only a matter of understanding what you can control, reviewing your strategy, and tapping into tools that will help your company thrive in this unfamiliar landscape.

With SimplyHRA, any business can take advantage of ICHRA to design cost-effective health insurance plans for employees. Use the visual dashboard for a bird's-eye view of your plans, set up benefits in minutes, and eliminate the middleman while providing your organization with flexible healthcare options — and the peace of mind it deserves.

See SimplyHRA in action by booking a personalized demo here. Good luck!

Related blogs

Should I Buy a Pre-Funded ICHRA Debit Card? 2026 Guide

How Employees Reconcile APTC After Joining Employer HRA 2026