ICHRA vs ACA Subsidies: Can You Keep Premium Tax Credits if Your Employer Offers an HRA?

TL;DR

ICHRA and premium tax credits (PTCs) are both affordable healthcare options for employees. If an employer offers an ICHRA that complies with the ACA affordability rule, employees are ineligible to claim PTCs and get subsidized healthcare.

Key takeaways

- Affordability requirement for large employers: Applicable Large Employers (ALEs) with 50 or more Full-Time Equivalent (FTE) employees are required to observe the affordability rule.

- ACA affordability threshold: Under the affordability rule, employee contributions for plan year 2026 should not exceed 9.96% of their household income.

- Opting out of ICHRA for PTC: If a small employer's ICHRA plan is deemed unaffordable, employees are allowed to opt out and claim PTCs instead.

With the cost of premiums skyrocketing, the search for better alternatives to traditional healthcare plans is more important than ever. And in search for a plan that balances coverage and affordability, a growing number of businesses are looking towards Individual Coverage Health Reimbursement Arrangements (ICHRA).

However, not everyone is open to the idea.

Some prefer more "tried-and-tested" options like utilizing premium tax credits (PTCs) to pay for their healthcare.

The problem arises when employers start to offer ICHRA (or any other HRA) while employees are more concerned about losing their subsidies.

We've seen questions such as: "Do I have to participate in my employer's HRA?" and "Will I lose my ACA credits if I use ICHRA?"

In this post, we'll address all of these questions one by one.

But first, a quick introduction.

What is ICHRA?

ICHRA is an HRA or Custom Health Option and Individual Care Expense (CHOICE) Arrangement that prioritizes flexibility and employee choice.

Under ICHRA, employees are free to choose their own individual health insurance plan. They can also use their reimbursement allowances to pay for eligible medical expenses, like dental visits, prescription medication, and pediatric care.

For employers, ICHRA offers complete cost predictability and ease of administration. You also don't have to worry about maximum or minimum (for small employers) contribution limits.

And similar to traditional group health plans, ICHRA plans are fully tax-advantaged (tax-free reimbursements and tax-deductible employer contributions).

Who Qualifies to Offer or Use ICHRA?

Any business, regardless of size, can use ICHRA to provide flexible and tailored healthcare to its employees.

Even a startup with just one Full-Time Equivalent (FTE) employee can use ICHRA, provided they're a W-2 employee and not partners (in a partnership), sole proprietors, or S corporation owners.

In terms of employee eligibility, the IRS defined a list of 11 approved employee classes that can be covered by ICHRA:

- Full-time employees

- Part-time employees

- Salaried employees

- Hourly employees

- Temps or employees from staffing firms

- Seasonal employees

- Employees under a Collective Bargaining Agreement (CBA)

- New employees within the waiting period (up to 90 days)

- Foreign employees working abroad

- Employees based on different rating areas

- Any combination of the classes above

Remember, these employee classes aren't defined solely for determining eligibility. Employers can also use these classes to set customized reimbursement allowances based on each employee group's health needs and risks.

This adds to the flexibility of ICHRA plans and how they can benefit both employers and employees.

What are the Cons of ICHRA?

While ICHRA looks like the best-case scenario for adjusting to burgeoning healthcare costs, there are a few disadvantages you should know about:

- Requires a more hands-on approach in employee education — While employees are ultimately in charge of plan selection under ICHRA, employers (and, if applicable, brokers) are responsible for educating employees about the mechanisms of their plan.

- Planning and administrative learning curve — Prior to switching from a traditional group health plan, employers need to conduct in-depth research on compliance (for Applicable Large Employers or ALEs), allowance modeling, and plan administration.

- Initial employee pushback — Despite gaining popularity in recent years, ICHRA is a new concept for a lot of employees, which sometimes leads to the perception that their healthcare is being "downgraded" for cost savings.

Aside from these cons, employees participating in ICHRA cannot claim PTCs. This can leave some employees feeling "stuck between a rock and a hard place," especially with limited knowledge of how ICHRA works.

This begs the questions, is ICHRA better than PTCs — or is it the other way around?

Should employees give up their current ACA subsidies to make the switch?

The answer isn't as cut-and-dried as it seems.

ICHRA vs Subsidized Healthcare: What to Choose?

To answer this question, we need to talk about two things: ICHRA affordability and PTC subsidy calculations.

First, employees don't have to worry about automatically losing their PTC just because employers start offering ICHRA.

If their employer's ICHRA is considered "unaffordable," they can choose to opt out of the plan and keep using their ACA subsidies.

The ICHRA Affordability Rule

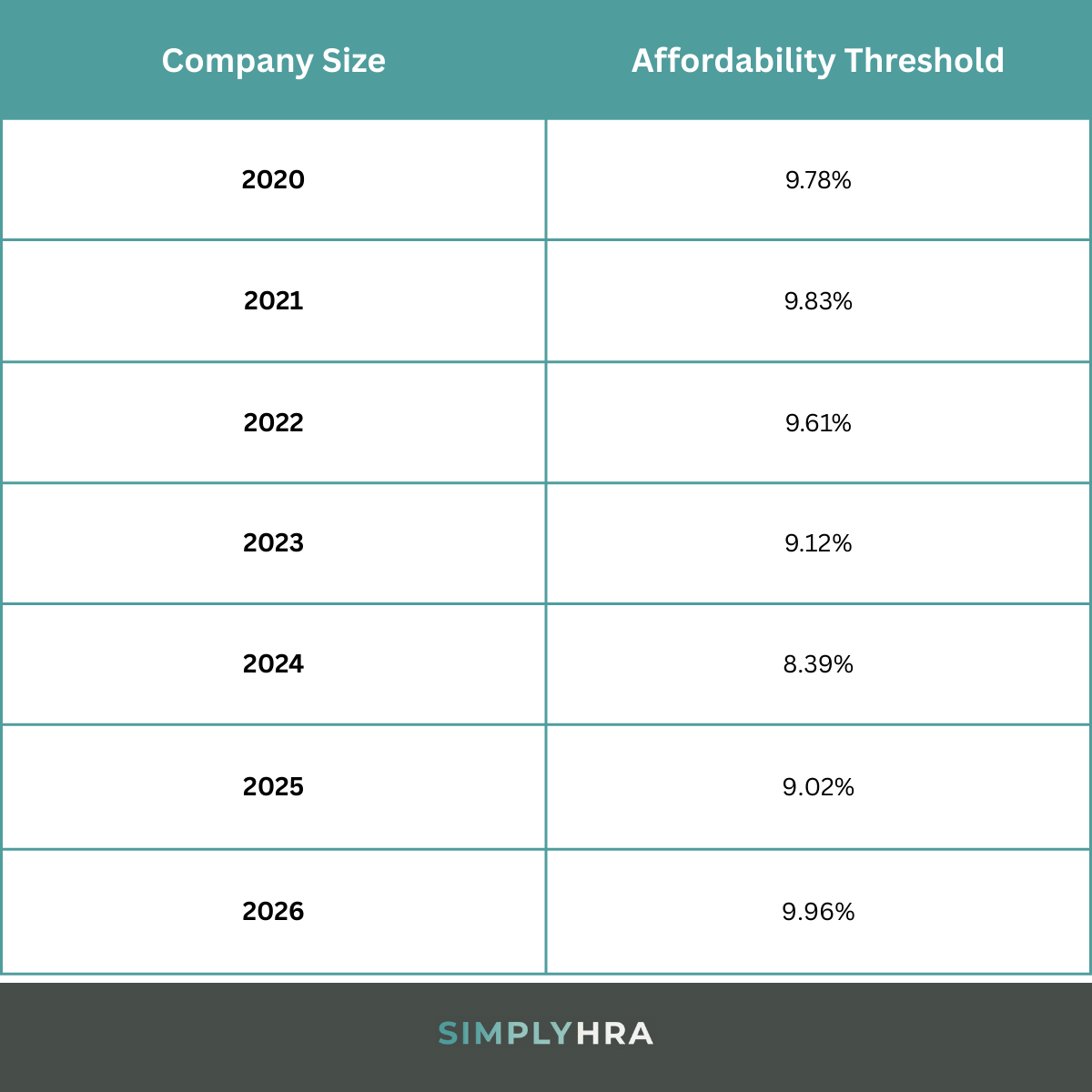

Under the IRS affordability rule, ALEs must make sure employee contributions to insurance premiums don't exceed 9.96% of their annual household income.

The affordability threshold changes every year:

Small employers (fewer than 50 FTE employees) aren't legally obligated to follow the affordability rule. As such, certain employee classes in their ICHRA may end up paying less for insurance with ACA subsidies.

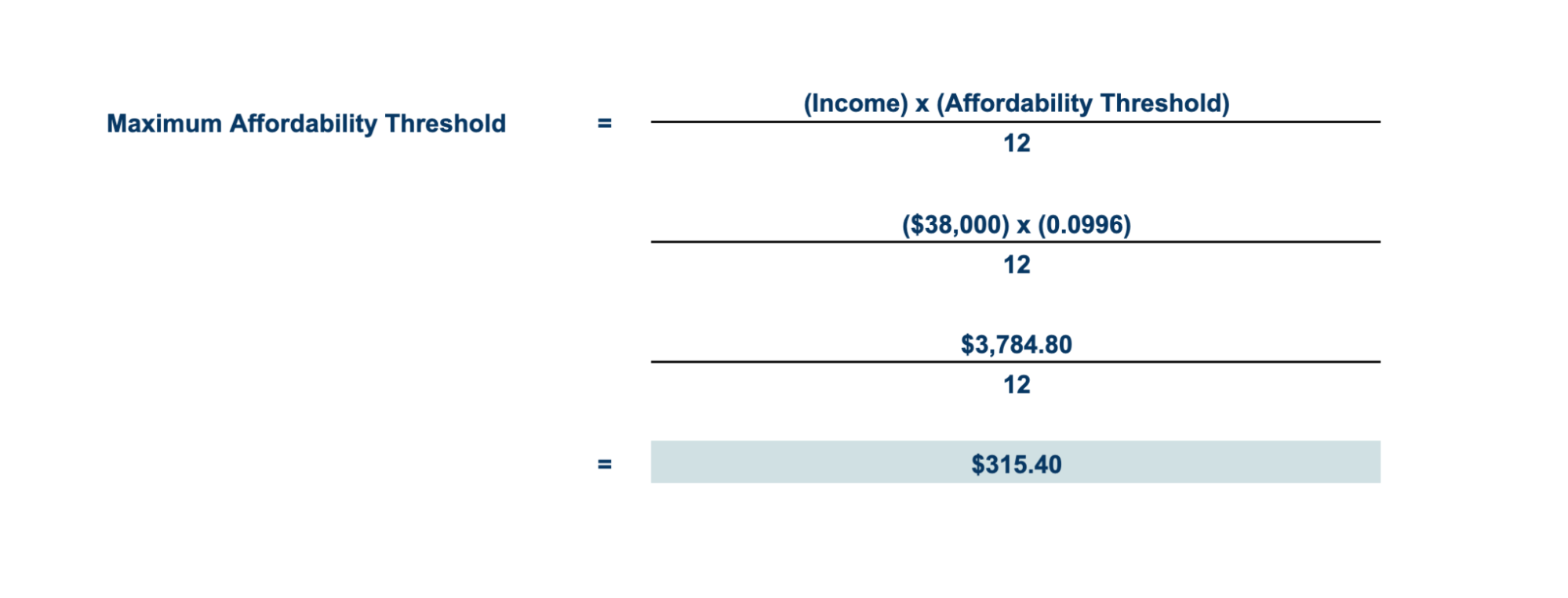

Let's say your employee's annual income is $38,000. Applying the 2026 affordability threshold, that means their contributions shouldn't exceed $315.40 per month — otherwise, the ICHRA will be considered "unaffordable."

If the Lowest-Cost Silver Plan (LCSP) in their area is $750, that means employers should cover — at the very least — $434.6 through ICHRA to make it affordable.

For example, if the ICHRA amount is only $400 per month, that means employees need to pay $350 per month out-of-pocket to pay for the LCSP, which costs $750. Since $350 is well beyond their affordability threshold of $315.40, the ICHRA plan is deemed unaffordable, giving employees the option to opt out and use PTC instead.

But, if the ICHRA reimburses $500, that means employees only need to pay $250 out-of-pocket for the LCSP. That's below their affordability threshold, meaning the ICHRA plan is affordable, and employees won't be eligible for PTC (even if they decline).

Employee Contributions with ICHRA vs PTC

The next question is, would ICHRA or PTC subsidies lead to more savings for employees?

As employers, this is an important and often-missed blind spot. Even if your ICHRA is affordable, sometimes employees (especially those in different states) would've received a higher amount from ACA subsidies.

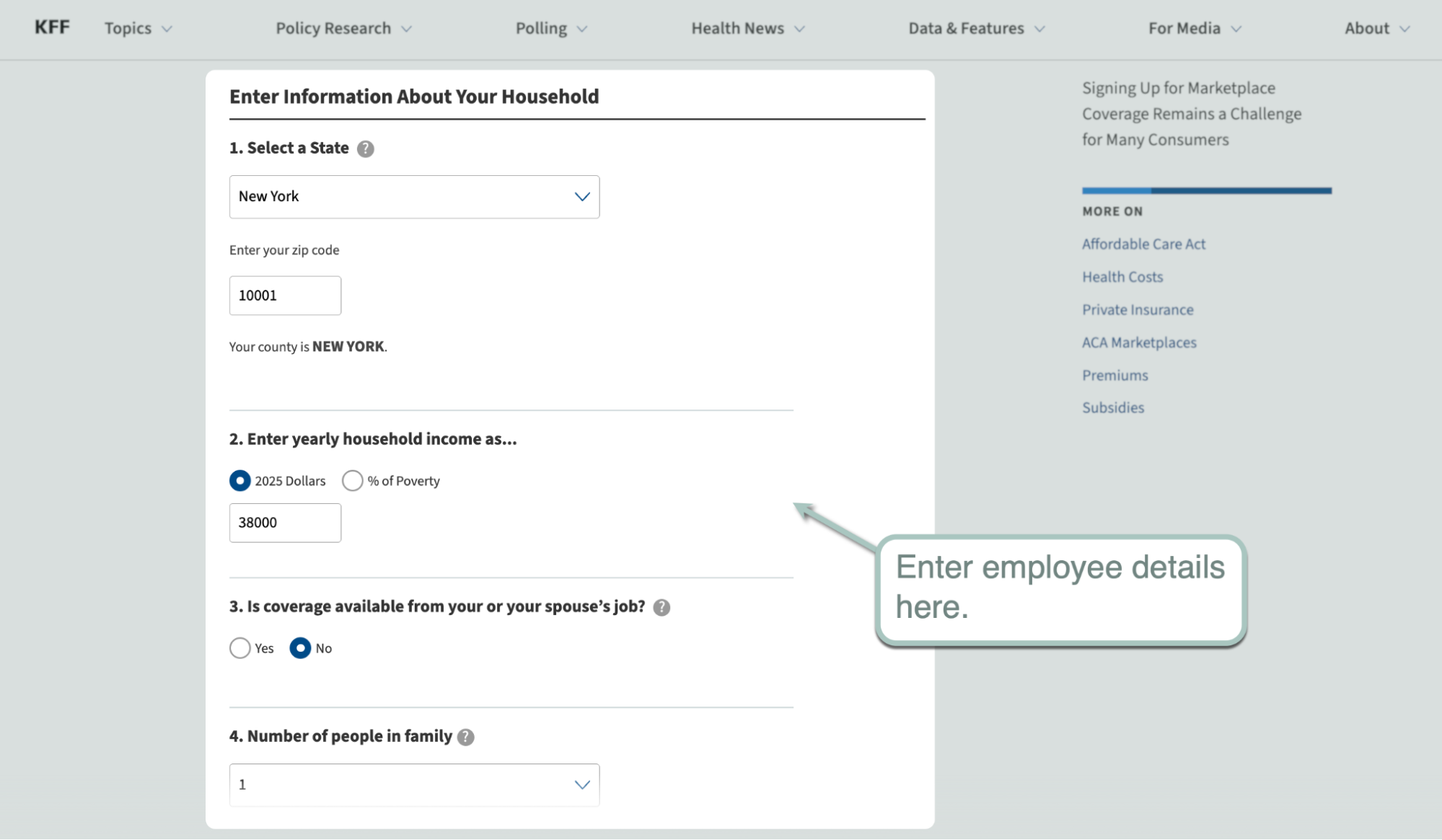

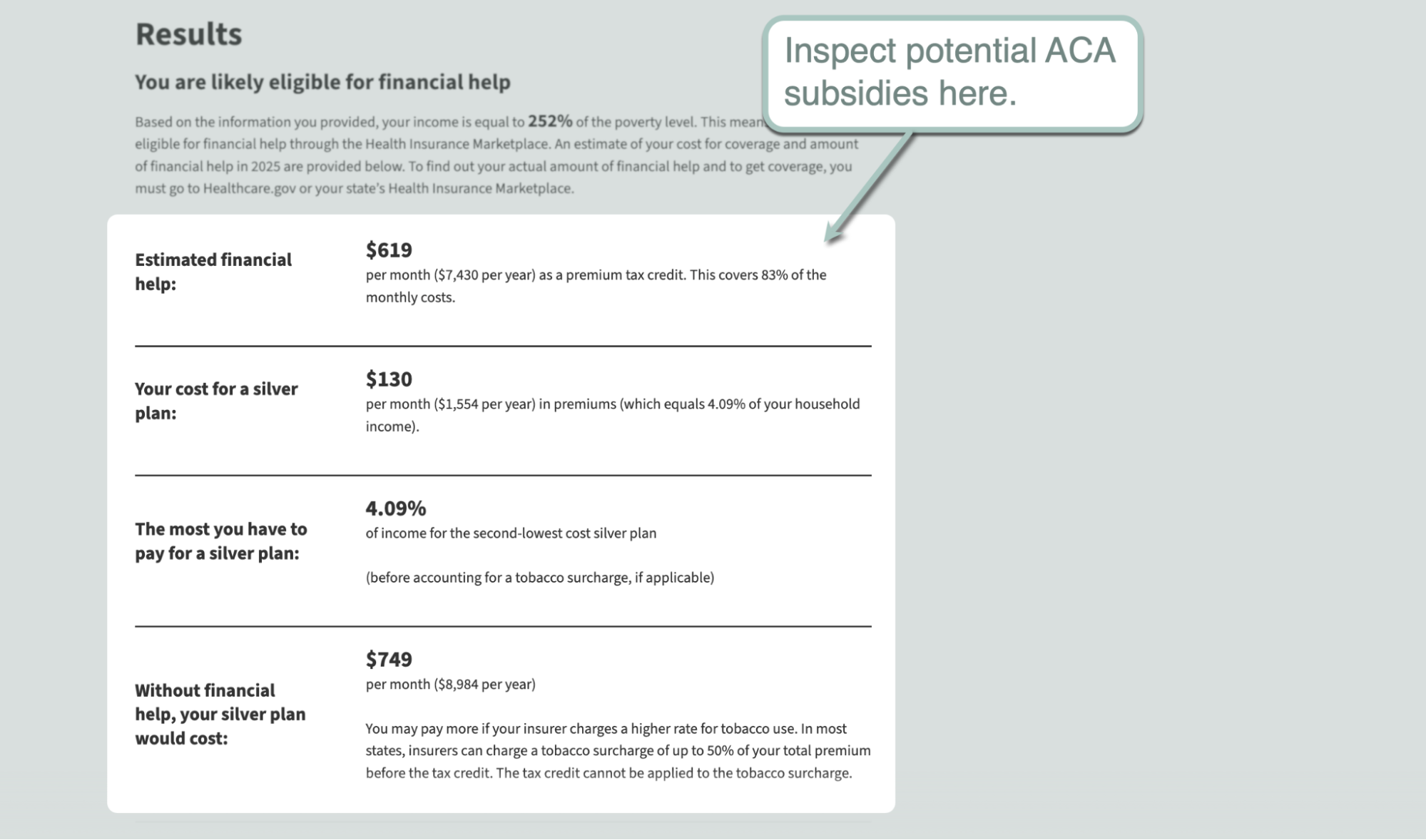

For this, use PTC calculators like the Subsidy Calculator by KFF. Just key in your employees' details, like their annual salary and zip code, and click 'Submit.'

Once the results are in, you'll find out how much they would've received in ACA subsidies and how much they have to pay out-of-pocket.

Use this information to formulate an allowance model that ensures your employees can get more out of ICHRA than ACA subsidies. If not, forcing them to your ICHRA — regardless of affordability — can be seen as a cost-saving move at the employees' expense.

As an employee, use this calculator to check if you're better off with PTC or ICHRA. Just remember that you need to make your final decision before the ICHRA plan's start date.

TL;DR

- If the ICHRA plan is unaffordable, only then will employees have the option to decline and use PTC.

- If the ICHRA plan is affordable, employees are no longer eligible to claim PTC.

- Only ALEs are required to follow the ICHRA affordability law.

- Just because an ICHRA is affordable doesn't mean it's more preferable to employees (if they could've gotten more through PTC).

As business owners looking to benefit from ICHRA's flexibility, predictability, and tax advantages, it's your responsibility to ensure employee satisfaction.

Your ICHRA may be deemed affordable, but you should also consider the ACA subsidies your employees would get. Forcing them to participate in an "affordable" ICHRA plan and give up higher PTC can be harmful, especially if you're after the other advantages of quality healthcare for employees (e.g., higher employee satisfaction, better health, and increased productivity).

The Case for ICHRA: Benefits for Employees

Suppose your employer's ICHRA offers the exact same as you would receive from ACA subsidies.

What other benefits can you expect from this new plan?

Here are some of the advantages of ICHRA that you won't get with ACA subsidies:

- Reimbursements for qualified medical expenses: Outside of individual insurance premiums, ICHRA funds can also be paid towards eligible medical expenses. This can be a huge advantage for employees over PTC, which can only be used to pay for health insurance premiums.

- Higher allowance ceiling: Generous employers can offer ICHRA reimbursement allowances that far exceed ACA subsidies — thanks to the fact that ICHRA plans don't come with annual contribution caps. In contrast, PTC is a fixed amount based on factors like your annual household income, number of dependents, and tobacco usage.

- Easy portability: Both Marketplace plans and plans purchased through ICHRA are portable. However, you might end up paying back your PTC come tax time if you get a higher-paying job.

ICHRA vs ACA Subsidies: Frequently Asked Questions

What to do when my employer stops offering ICHRA?

If your employer decides to discontinue ICHRA for any reason, your first step should be to report a Qualifying Life Event (QLE) through your Marketplace portal. This will trigger a Special Enrollment Period (SEP) that will help you secure your coverage and reapply for ACA subsidies.

Will my coverage stay intact if I switch from ICHRA to ACA subsidies?

If your employer's ICHRA is unaffordable, you can opt out of the plan and switch to using PTC without affecting your current health coverage. For this, you need to update your Marketplace account and pay through the client portal or choose a new plan.

Should you elect COBRA if your ICHRA plan is discontinued?

Employees may be offered to elect COBRA — short for "Consolidated Omnibus Budget Reconciliation Act" — to keep certain features of their ICHRA for a limited time (useful if you have money in your Health Wallet or ongoing treatments). Just remember that you have to pay the employer's previous contribution on top of a 2% administration fee, not to mention that you can't claim PTC if you're actively using COBRA. In most cases, electing COBRA isn't worth it if you're coming from ICHRA since you already own your health plan and can simply pay directly while using ACA subsidies.

Conclusion

Both ICHRA and ACA subsidies can help reduce healthcare costs for employees.

The question of which option is better depends on factors like the ICHRA allowance, PTC amount, local premium prices, and whether you're eligible for ACA subsidies in the first place.

It's also important to investigate the structure of your ICHRA plan, including other benefits like ease of administration, flexibility, and support for certain medical expenses beyond just insurance premiums.

Just remember, you can't use ICHRA and claim PTC at the same time. Whatever you choose, make sure you finalize your decision before the ICHRA plan's start date.

If you have other questions, don't hesitate to reach out to us here. Cheers!

Related blogs

ICHRA Adoption in 2026: The Complete Guide for Employers

Affordable ICHRA Solutions for Under 50 Employees: 2026