The Step-By-Step ICHRA Implementation Guide for 2026

Individual Coverage Health Reimbursement Arrangements (ICHRAs) are on the rise. And for those who understand how it works, it's no surprise.

Annual premium hikes, time-consuming processes, ineffective "blanket" plans for a diverse workforce — it's time to put these headaches in the past.

Let us walk you through everything there is to know about ICHRA, including how it works, why it's a game-changer, and what to do for a successful implementation.

1. What is ICHRA?

Individual Coverage Health Reimbursement Arrangement (ICHRA) is an employer-sponsored health benefit structure finalized in 2019 and launched on January 1st, 2020.

Under ICHRA, employers set monthly reimbursement allowances that can be used to pay for individual health insurance premiums and other qualifying medical expenses.

Sounds simple enough, right?

What really sets ICHRA — as well as other HRAs — apart is the aspect of employee choice.

Put simply, ICHRA allows employees to choose:

✅ Which individual health insurance plan to purchase (on and off the ACA marketplace)

✅ What insurance carrier to buy from (UnitedHealthcare, Blue Cross Blue Shield, Kaiser Permanente, etc.)

✅ Whether to include coverage for dependents (and whom)

✅ Whether to use their reimbursement allowance for specific out-of-pocket health services and expenses

✅ The metal level that suits their needs and budget

1.1 ICHRA 2025 Statistics

ICHRA adoption statistics

- ICHRA adoption among small businesses is up 52% year over year

- For larger businesses, adoption is up 34%

- For businesses with 100-199 employees, adoption is up 50%

More than 83% of ICHRA adopters in 2025 previously offered zero coverage

In 2025, roughly 70% of ICHRA enrollees chose Silver or Gold plans

By 2030, the US Treasury Department predicts that 800,000 employers will offer ICHRA, covering more than 15 million employees

Where employers learn about ICHRA

- 51% — ICHRA vendor or administrator representative

- 35% — The organization's health benefits consultant

- 32% — Health insurance conference and other learning events

- 25% — Online resources and trends

- 20% — Social media (primarily LinkedIn)

1.2 How ICHRA Compares with Other Plans

ICHRA

QSEHRA

Traditional Group Plans

Employer size eligibility

No limits

Only for companies with <50 employees

At least 2 FTE employees (for small group health plan), 70% participation requirement

Contribution limits

No minimums, no maximums

Capped at $6,350 per year ($12,800 for families)

Premiums dictated by carrier

Employee choice

Full control (any individual plan on and off the ACA marketplace)

Full control (similar to ICHRA)

Very limited

Tax benefits

100% tax-deductible, tax-free reimbursements

100% tax-deductible, tax-free reimbursements

Pre-tax premiums, tax-free benefits

Predictability and costs

100% fixed contribution amounts

100% fixed contribution amounts

Unpredictable annual rate increases

2. How Does ICHRA Work

It's worth noting that, under ICHRA, employers don't directly give cash to enrolled employees. Rather, they set monthly reimbursement allowances for health insurance premiums and other qualified medical expenses.

Employees will take care of the rest — choosing an individual health insurance plan, paying premiums upfront, and submitting receipts to get tax-free reimbursements.

Note: Employers can set different reimbursement allowances per employee class (e.g., full-time, part-time, seasonal, and non-salaried).

ICHRA for Employers

ICHRA ensures cost predictability, tax-deductible contributions, and reduced administrative burdens. Platforms like SimplyHRA also take away paperwork-related headaches, be it in plan management or compliance. You can also take advantage of workflow automation tools, saving money on HR headcount and avoiding costly human errors.

ICHRA for Employees

ICHRA puts employees in the driver's seat in terms of plan selection. Rather than a blanket solution that barely works for everyone, you can build a plan that's perfectly suited to your healthcare needs. In addition to your individual health insurance premiums, you can also use your ICHRA allowance for a list of eligible medical expenses (e.g., prescription drugs, vision exams, physical therapy, and maternity care).

2.1. Understanding ICHRA Workflow

- Setting Up Your ICHRA Plan — Use a benefits platform like SimplyHRA to specify employee classes and assign monthly reimbursement allowances.

- Integrating Existing Medical Plans — Employees with current eligible plans add their healthcare benefit information and choose a payment strategy.

- Choosing a New Plan — Employees can purchase a new plan straight from the SimplyHRA dashboard.

- Creating a SimplyHRA Virtual Card or Bank Account — Employees can choose to use a SimplyHRA virtual card or bank account for automatic payments (requires SimplyHRA Premium).

- Manual Payment — For employees who opted out of auto-payment, they need to add and verify their own payment method.

- Submitting Reimbursement Requests — Employees send reimbursement requests by attaching receipts, insurance bills, and other proofs of payment.

- Reimbursement Payouts — Reimbursements are approved and manually or automatically (requires SimplyHRA Premium) added to the employee's payroll.

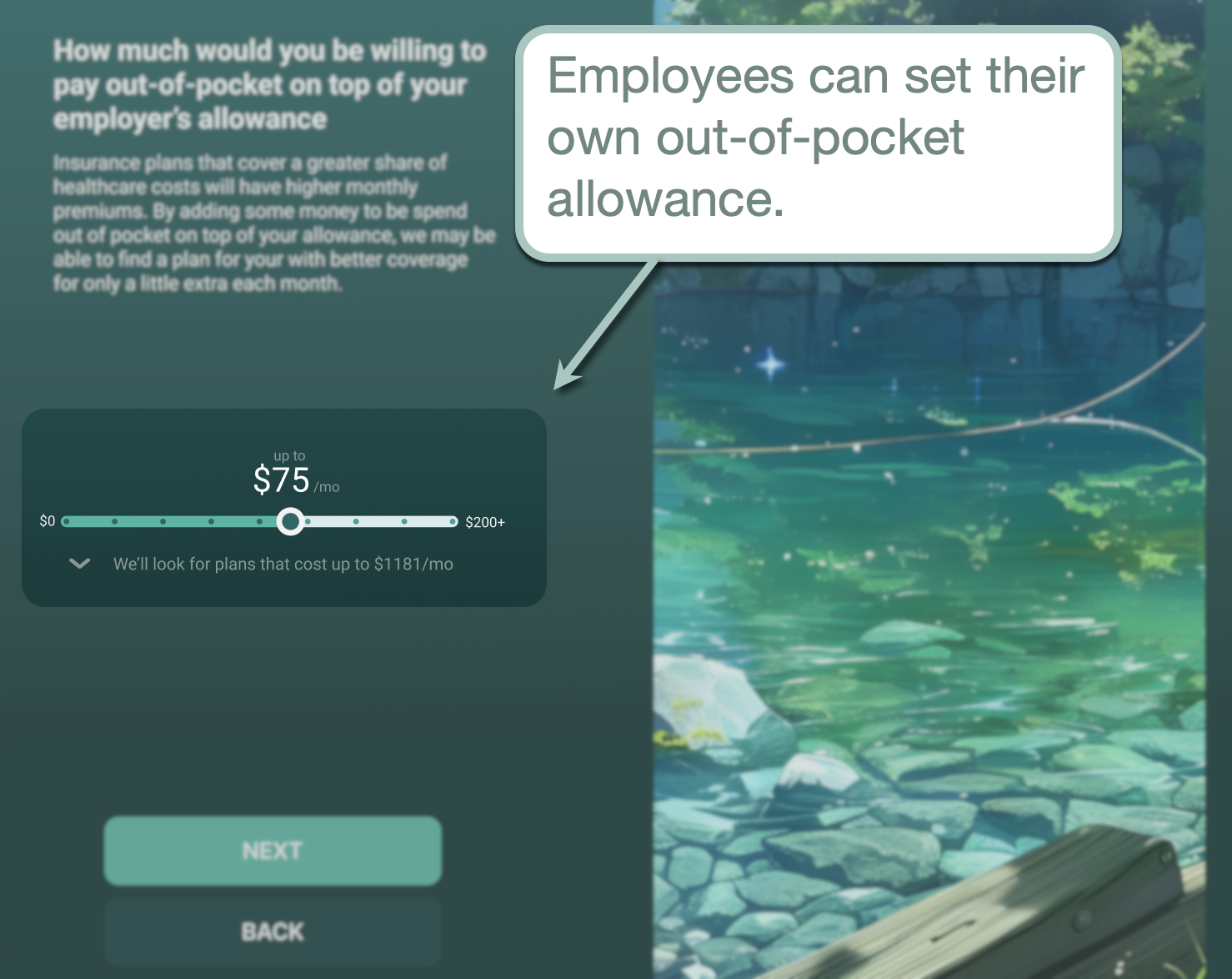

Tip: Employees can set an amount to add on top of their ICHRA reimbursement allowance, enabling them to find plans with better coverage through SimplyHRA. This is a crucial step in the employee onboarding process.

2.2. Practical Benefits of ICHRA

- Easy administration. Modern ICHRA platforms can help you set up reimbursement plans in minutes while taking advantage of automation features to streamline employee healthcare.

- Cost control and predictability. Set your own monthly reimbursement allowances for employees with zero surprise rate increases.

- Employee choice and satisfaction. ICHRA lets employees choose from individual health insurance plans (including dental and vision care) that perfectly match their needs.

- No limitations and participation requirements. Every business is eligible to use ICHRA regardless of size and employee participation rate.

- Tax benefits. ICHRA contributions are tax-deductible, while reimbursement payouts are completely tax-free.

The SimplyHRA Advantage

Your ICHRA plan is as good as your chosen benefits platform. And with SimplyHRA, there's a lot to love:

Done-For-You Compliance

Just focus on creating ICHRA plans your employees deserve and leave the time-consuming, compliance-related tasks to us.

Integrated AI Chat Assistant

Simplify employee onboarding and training with a 24/7 AI chatbot that instantly provides direct answers to any question.

Automation Tools

Set up automatic approval workflows, expense tracking, reporting, reimbursements, and more.

No Bank Application Needed

Create a SimplyHRA debit account, virtual card, or physical card directly from the app.

3. When ICHRA Makes Sense

ICHRA is ideal for the following company profiles:

- Geographically diverse teams — Unlike traditional group plans that use the most expensive state as a baseline, ICHRA allows you to tailor your reimbursement budget for each employee's location.

- High-turnover companies (e.g., construction and staffing) — ICHRA is a fully portable plan that allows employees to keep their insurance policies even after transitioning from your company.

- High renewal costs — ICHRA removes your dependency on carrier-driven renewal hikes that cause companies to bleed money.

- Mixed employment setups — ICHRA makes it easier to create custom plans for employees with different employment classifications (e.g., part-time, full-time, seasonal, and contract-based).

- Just above the small employer classification — Companies with 50-500 employees (just hit the ACA employer mandate) can switch to ICHRA to avoid unpredictable group premiums and other expensive insurance rules.

- Professional services firms — When planning healthcare budgets, ICHRA enables law firms, tech agencies, financial services, and other professional service providers to factor in different roles and seniority levels (i.e., associates and support staff).

Can You Offer ICHRA Alongside a Group Plan?

Yes, but not to the same employees. You must also abide by ICHRA class size requirements:

- Fewer than 100 employees: Your ICHRA class must have at least 10 participants.

- 100-200 employees: Your ICHRA class must include at least 10% of all employees.

- More than 200 employees: Your ICHRA plan must include at least 20 employees.

Who Can Offer ICHRAs to Employees?

Any employer can offer ICHRA, even those with only one employee. This doesn't apply if the person is a self-employed owner or their spouse.

4. ICHRA Implementation: Step By Step

4.1. Understand Your Healthcare Goals

Start by deciding how much money your company can reasonably commit to employee benefits each year.

The good news is, any amount you choose at this stage will become your fixed, predictable cost.

Put your budget into perspective by understanding the pain points with your current employee health plan.

Are employees concerned about the costs or lack of choices? Are they informed enough to make decisions about their individual health insurance?

These questions will not only help you set an adequate budget for your ICHRA strategy. It also allows you to refine your employee onboarding and training plan, which can benefit from tools like SimplyHRA's AI assistant.

Action Plan:

- Compile employee details into a census.

- Organize your team into employee groups.

- Obtain employee input and understand their healthcare needs.

- Decide on a budget that can cover those needs.

4.2. Build Your Allowance Model

The next step is to plan your allowance model, which pertains to the allocation of your ICHRA funds across employee groups.

Remember, ICHRA doesn't have maximum contribution amount requirements. But with your overarching budget set, it's just a matter of understanding employee classifications:

IRS-Approved ICHRA Classes

- Full-Time Employees — Workers who put in 32-40+ hours per week.

- Part-Time Employees — Any employee doing fewer hours than your full-time workers.

- Seasonal Employees — Hired for temporary roles that generally last 6 months or less.

- Employees covered by a bargaining agreement — Employees covered by a Collective Bargaining Agreement (CBA).

- Employees who haven't cleared the waiting period — Newly-hired employees in the permissible waiting period, no longer than 90 days.

- Non-resident aliens with no US-sourced income — Foreign employees who don't reside in the US.

- Employees who primarily work in a specific rating area — Location-based employees by ACA rating area or state.

- Salaried employees — Fixed income earners.

- Non-salaried employees — Workers paid on an hourly, shift-based, or piece-rate basis.

- Employees engaged through a staffing firm — Temp agency and PEO-leased workers.

- Any combination of two or more of the classes above.

ICHRA Affordability Rule 2026

For an Applicable Large Employer (ALE), make sure your employees' share of their monthly premiums (after ICHRA) doesn't exceed 9.96% of their annual household income.

4.3. Creating your ICHRA Plan Document

Compile the following details into an ICHRA Plan Document and a shorter Summary Plan Document (SPD):

Basic Information

- Official plan and employer name

- Employer EIN

- Plan year

- ICHRA plan tools, services, and administrators

Eligibility

- ICHRA employee eligibility requirements

- New hire waiting periods

- Dependent eligibility

- Verification frequency

Benefits

- Plan benefits overview

- Eligible healthcare expenses (outside of health insurance premiums)

ICHRA Transactions

- Reimbursement request and claims procedures

- Reimbursement document requirements

- Reimbursement deadlines

- Processing timeline

Plan Amendments and Security Provisions

- Privacy officer designation

- Employee privacy rights

- Medical document storage rules and policies

- Plan amendment and termination procedures

Disclosures

- All applicable laws

- Employee Retirement Income Security Act (ERISA) rights statement

- Non-discrimination rules

- Right to appeal and procedures

- Final decision timeline and process

Have Questions?

Contact us here, and we're happy to walk you through the process.

Remember that SimplyHRA customers can breeze through the plan setup and compliance aspects of ICHRA — we'll do the heavy lifting for you!

4.4. Start Onboarding

Your budget is set, and so are your employee classes.

It's time to start onboarding your employees.

This technical side of this process largely depends on the benefits platform you choose. However, there's also the leadership side that focuses on getting employees prepared for the transition.

Important: Companies are required to send a 90-day initial notice before the beginning of the next ICHRA plan year.

Prioritize the following topics in your ICHRA onboarding communication:

- Employee classes — How are ICHRA employee groups determined, and what are the factors considered?

- Reimbursement amounts — What are reimbursement allowances, and how are they calculated?

- Plan selection process — How to choose a health plan using your ICHRA platform?

- ICHRA timeline — When is the enrollment deadline and plan start date?

Onboarding Techniques for Employees

Remember, the success of the onboarding process relies on effective communication, which may involve different methods depending on the employee.

- One-on-one sessions between brokers and employees

- Hosting live, replayable webinars

- Online resources (e.g., FAQ page, checklists, and online video tutorials)

- Personalized "allowance letters" or countdown emails

- Printed quickstart guides

- Side-by-side comparison material between ICHRA and the old plan

4.5. Set Up Payments

It's not uncommon for small businesses to handle reimbursement payouts for their HRA manually. However, this is a highly burdensome process that can worsen as the company scales.

In modern ICHRA, implementing payment automation systems is the way to go.

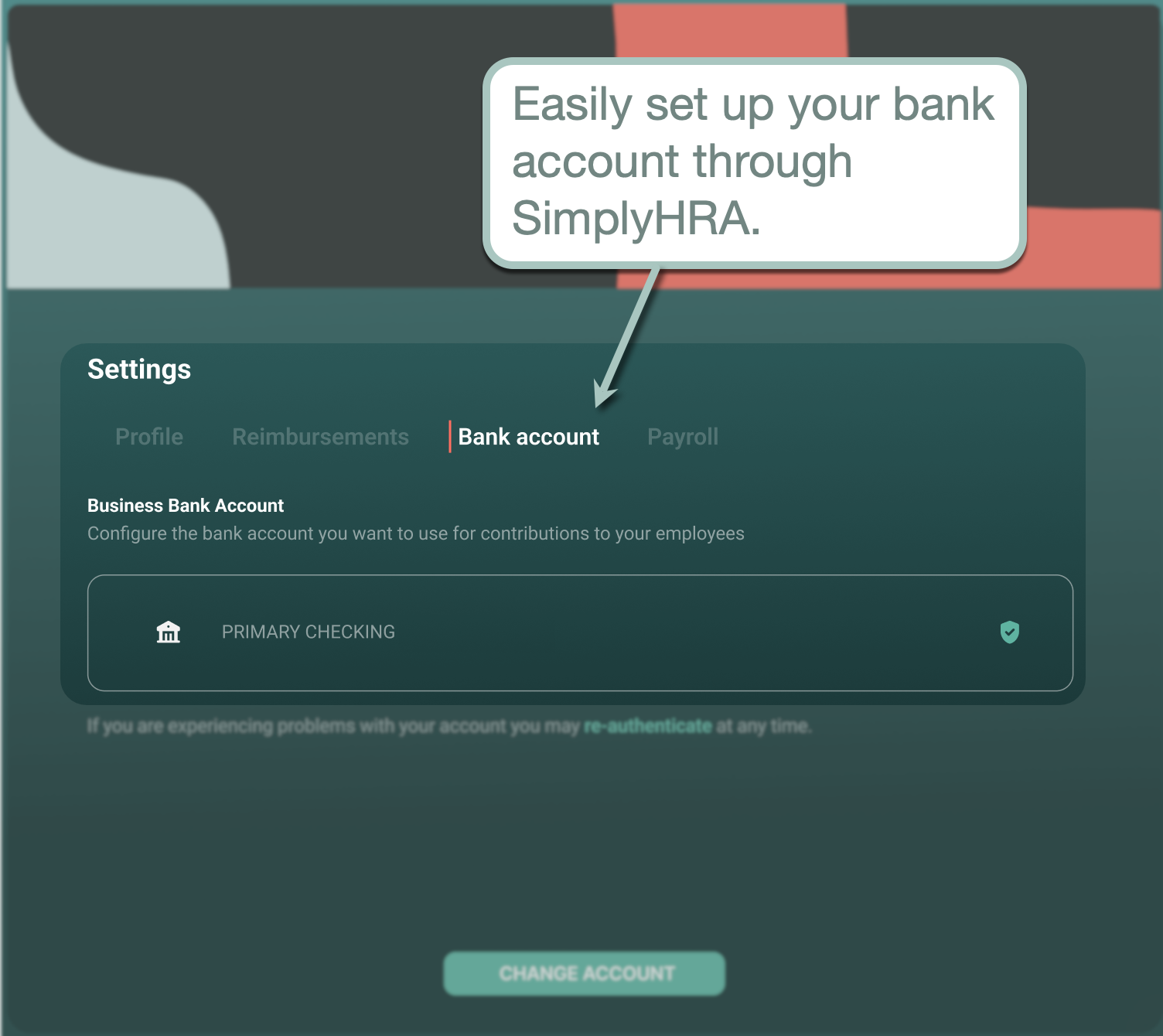

With SimplyHRA, employees are in charge of submitting reimbursement requests, while approvals and payouts will be automated. Your primary involvement as an employer is to simply connect your business bank account, which will be used for contributions.

How to Set Up Your Bank in SimplyHRA:

- Step 1: Click 'Settings' from the main side panel.

- Step 2: Switch to the 'Bank account' tab.

- Step 3: Connect your account and complete any required verification steps.

4.6. Compliance Checklist

- Ensure the plan is offered only to 11 IRS-approved employee classes.

- Minimum class size met (when offering ICHRA alongside a group plan).

- Send a written ICHRA initial notice 90 days before the plan year.

- For ALEs, make sure employee premium contributions don't exceed 9.96% of their annual household income.

- Create an ERISA-compliant ICHRA Plan Document and SPD (two different documents).

- File Form 1095-B and 1094-B (for small employers), Form 1095-C and 1094-C (for ALEs), and Form 720 before IRS deadlines.

- Learn existing IRS, ERISA rules (e.g., ERISA §510) and monitor for changes. Maintain a complete and clean record of all reimbursements, notices, and proof of coverage.

- Obtain initial proof of coverage from enrollees and verify monthly (participants must have individual health insurance or Medicare).

- Review compliance and records on year-end.

5. Choosing The Right ICHRA Partner

Understanding ICHRA is a crucial step towards more flexible, cost-effective, and dependable employee healthcare.

Next comes the most important decision in your ICHRA implementation plan: Who do you work with?

When assessing a benefits platform or third-party administrator, you need to look for the following:

Compliance Expertise

Compliance is a non-negotiable when offering ICHRA to your workforce. Make sure you work with people who verifiably and transparently know their way around matters like ERISA, HIPAA, IRS, and COBRA rules (better yet, who can handle all compliance-related stuff on your behalf).

Streamlined Process

Choose a TPA or benefits platform with an intuitive, clutter-free administration interface that makes key tools and features easy to find. Support for automation tools (e.g., approvals and reporting) is a huge plus.

Employee Support Tools

Go for a solution that your employees can learn and use from day one. Modern platforms like SimplyHRA offer a straightforward, app-like experience equipped with a 24/7 AI chat assistant — providing employees with instant answers and assistance for platform tasks (i.e., requesting reimbursement status updates).

Pricing Transparency

ICHRA platforms shouldn't get in the way of better, more predictable financial control through hidden fees and an obscure pricing structure. Look for a flat charge per employee with a reasonable platform fee.

Administration Support

Work with a team that can guide and assist you through the initial challenges of implementing ICHRA. SimplyHRA, for example, offers priority support, onboarding guidance, and in-house health benefits enrollment assistance.

Integrations

Lastly, choose a solution that helps streamline your software stack through ready-to-use system integrations. This can be with your payroll management or Human Resources Information System (HRIS), like Gusto, Plane, and ADP.

6. ICHRA: Frequently Asked Questions

Can employees participate in ICHRA without individual insurance?

No, employees need a qualifying individual insurance plan in order to receive reimbursements from ICHRA. The good news is that reimbursements are only paid out after employees submit their proof of coverage, ensuring you never pay for unused benefits.

Does ICHRA work with traditional group plans?

Although ICHRA can be offered alongside a traditional group plan, employees cannot participate in both benefits at once. Combining these plans in your organization also requires you to follow the minimum participation requirements for your ICHRA class.

Is it unfair to offer different benefits based on each employee's location or employment status?

No, it's generally not unfair to provide different reimbursement allowances, especially if you're considering buying power and the insurance price differences between states. This is why it's important to obtain a firm grasp on your workforce's healthcare needs and financial means when designing your ICHRA plan.

Can I dictate which individual insurance plans our employees get?

No, only employees have the authority to choose which individual insurance product to buy. Recommendation engines and brokers are only allowed to make suggestions — never to decide on the employee's behalf.

ICHRA Myths vs Facts

- Myth: Employees will struggle to find plans on their own — Truth: On the contrary, employees are better informed than their employers when it comes to choosing benefits that suit their specific needs.

- Myth: ICHRA plan is unattractive to new employees — Truth: Employees understand and believe in the value of choice when it comes to healthcare.

- Myth: ICHRA is only for small employers — Truth: ICHRA's rising popularity among medium-sized and large businesses proves its scalability (no maximum contribution and employee size limits).

- Myth: ICHRA is complicated — Truth: With a good benefits platform or TPA, ICHRA is arguably the easiest healthcare has ever been for businesses and employees alike.

Getting Started with ICHRA

Every successful ICHRA strategy is built on a key decision:

Who should I partner with?

Make the right choice, and everything else falls into place.

With SimplyHRA, our success metric is how satisfied you and your employees are with your ICHRA plan. We can help set up your ICHRA plan in minutes, provide in-house enrollment assistance, and communicate with each employee to discuss their options based on family size, health profile, budget, and more.

Get to know ICHRA by scheduling a personal demo here.

Contact Us

- Email — info@simplyhra.com

- Phone — +1 (909) 257-8030

- Address — 27 Mauchly Ave, Irvine, CA 92618

Related blogs

Handling Partial Reimbursements for Benefits: 2026 Guide

ICHRA Onboarding Checklist for New Employer Customers 2026